Silicon and Sympathy. Can the Bank of the Future Actually Be Your Friend?

Table of Contents

1. The Vending Machine and the Sherpa An introduction to why banking apps feel cold, and why the industry is desperate to simulate warmth.

2. The Architecture of Empathy (Retail Banking) In which an AI named “Lily” explains why you can’t afford that espresso, but does so gently.

3. The Invisible CFO (SME Banking) How the “Orchestrator” moves from nagging small business owners to saving them from themselves.

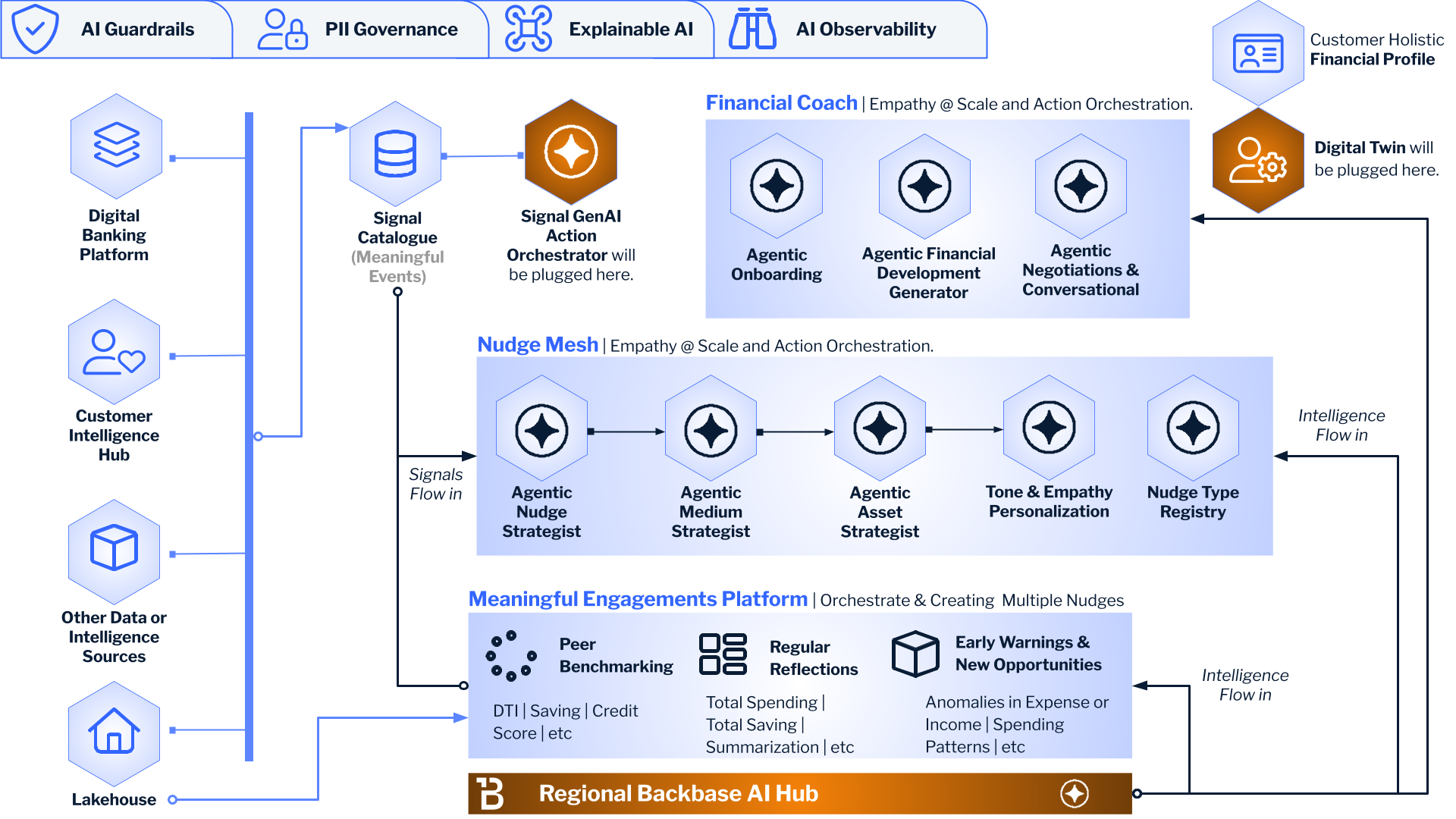

4. The Lakehouse and the Loom A look at the messy plumbing that makes the magic trick possible.

The Vending Machine and the Sherpa

For the better part of the last decade, logging into your banking app has felt less like visiting a trusted advisor and more like interacting with a vending machine that occasionally eats your dollar. You insert credentials; it dispenses a balance. It is transactional, binary, and largely indifferent to your existence. It is a relationship defined by the cold, digital silence of a spreadsheet — functional, yes, but devoid of the biological imperative to actually help you survive.

But if you look at the schematics currently circulating in the C-suites — specifically the blueprints for “Empathy at scale” and “Banking CLV Strategy” — a shift is occurring. The industry is tired of being a vending machine. They want to be something else entirely. They want to be Sherpas.

In my manifesto on the “Invisible Bank,” I argued that we are approaching the end of “banking as a chore.” The current state of the industry as a “Byzantine maze of 40-year-old core systems,” where AI models are like “chefs trying to cook a gourmet meal by sourcing ingredients from five different, locked pantries.” The result? A banking experience that is visible, heavy, and full of friction — the digital equivalent of standing in line behind a velvet rope just to ask for your own money.

The future, I believe is Invisible. It is a world where banking disappears into the background, managed by an autonomous “Financial Digital Twin” that negotiates your mortgage rates while you sleep. But invisibility is hard work. To make a bank disappear, you have to build a very large, very complex machine to replace it.

Traditional banking is like a library where all the books have been thrown in a pile on the floor. You know the information is there — your transaction history, your spending habits, your looming liquidity crisis — but good luck finding it. You are left to wander the stacks alone.

This new AI architecture, however, changes the physics of the room. It is not just a librarian; it is a librarian who has read every book, memorized your Dewey Decimal location, knows you are going through a messy breakup, and silently slides a copy of Eat, Pray, Love and a low-interest consolidation loan across the desk before you even ask.

The documents before us — a series of dense architectural diagrams, flowcharts, and interface mockups — are the wiring diagrams for this invisibility cloaks. They show us exactly how the sausage is made, or rather, how the “Data Mesh” (the ingredients) meets the “Customer Lifetime Orchestrator” (the chef) to serve up something that tastes surprisingly like empathy.

This is not just about automation; it is about “Augmentation.” Traditional automation is a “black box” that says no; this new architecture is a “glass box” — an Explainable AI that explains why. It is the difference between a smoke detector that beeps while your house burns down, and a smart sprinkler system that detects the heat signature of burning toast and puts it out before the curtains catch fire.

It’s the shift from “Here is a feature” to “Here is the context.”

Please keep on reading in https://www.linkedin.com/pulse/silicon-sympathy-can-bank-future-actually-your-friend-chris-shayan-qqelc/