For the banking sector, AI has transitioned from a “horizon technology” to an operational imperative. However, the gap between having AI initiatives and being an AI-mature organization is widening. While fintech disruptors often start at a high maturity level due to their lack of legacy debt, traditional financial institutions face a complex journey.

Drawing upon the Gartner AI Maturity Model, this article provides a framework to objectively assess your bank’s current AI capabilities and engineer a roadmap toward an “AI-First” operating model. This is not merely about deploying chatbots; it is about the systematic industrialization of intelligence across the balance sheet

[Download the Banking AI Maturity Assessment Tool Here]

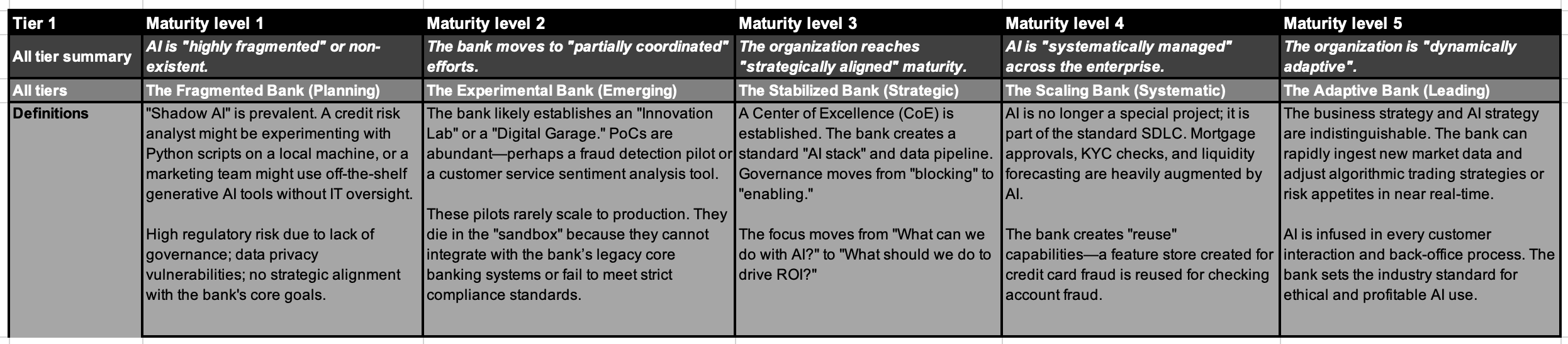

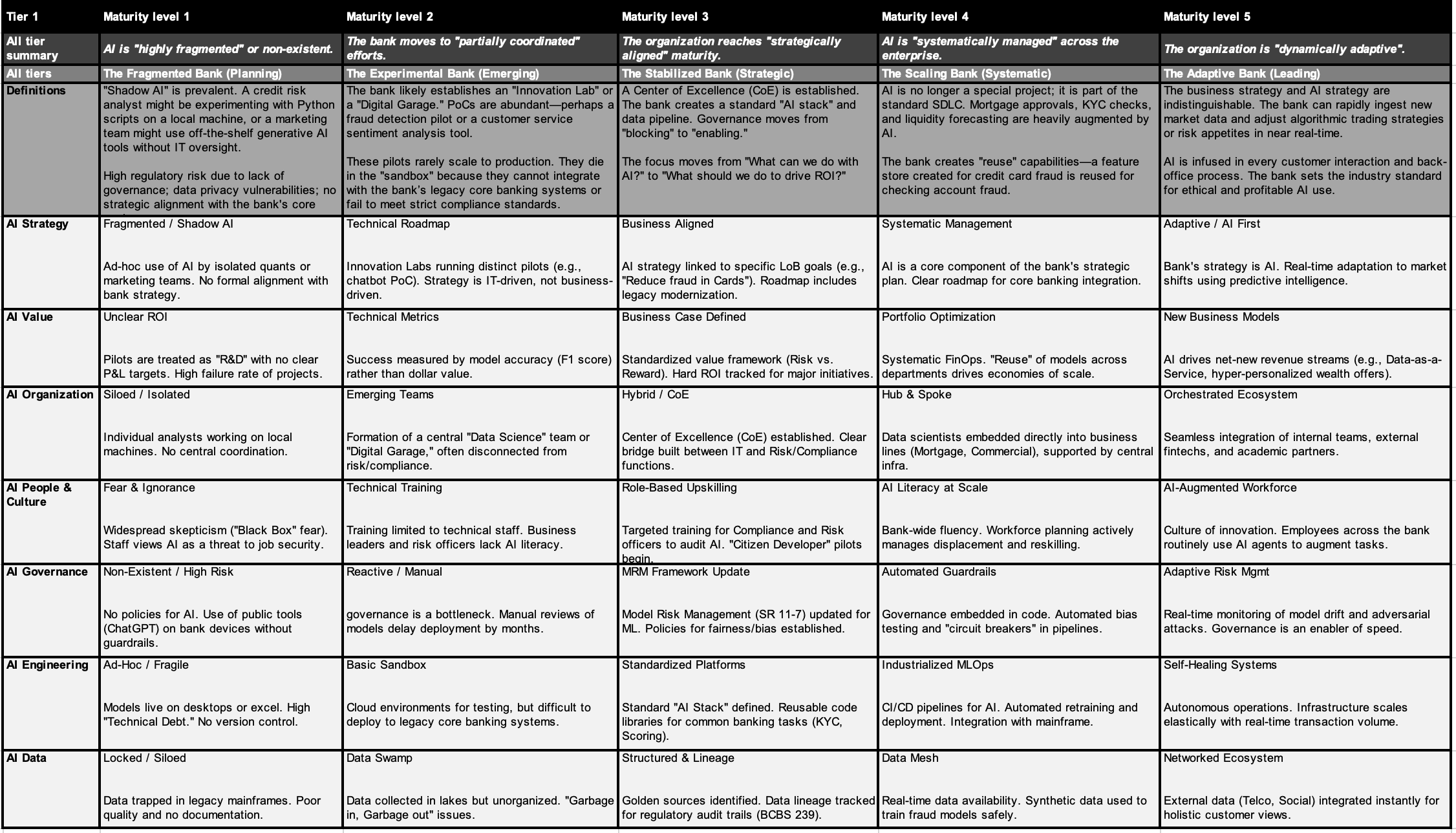

The Five Stages of Banking AI Maturity

The “AI tourism” in banking is over. While many financial institutions have successfully deployed isolated chatbots or fraud detection pilots, the challenge now shifts from experimentation to industrialization. According to the Gartner AI Maturity Model, true maturity is not measured by the number of models in production, but by the holistic integration of AI strategy, governance, and engineering into the fabric of the enterprise.

To understand where a bank stands, we must first define the trajectory. Based on the progression from Level 1 (Planning) to Level 5 (Leading), here is how these stages manifest specifically within a financial institution:

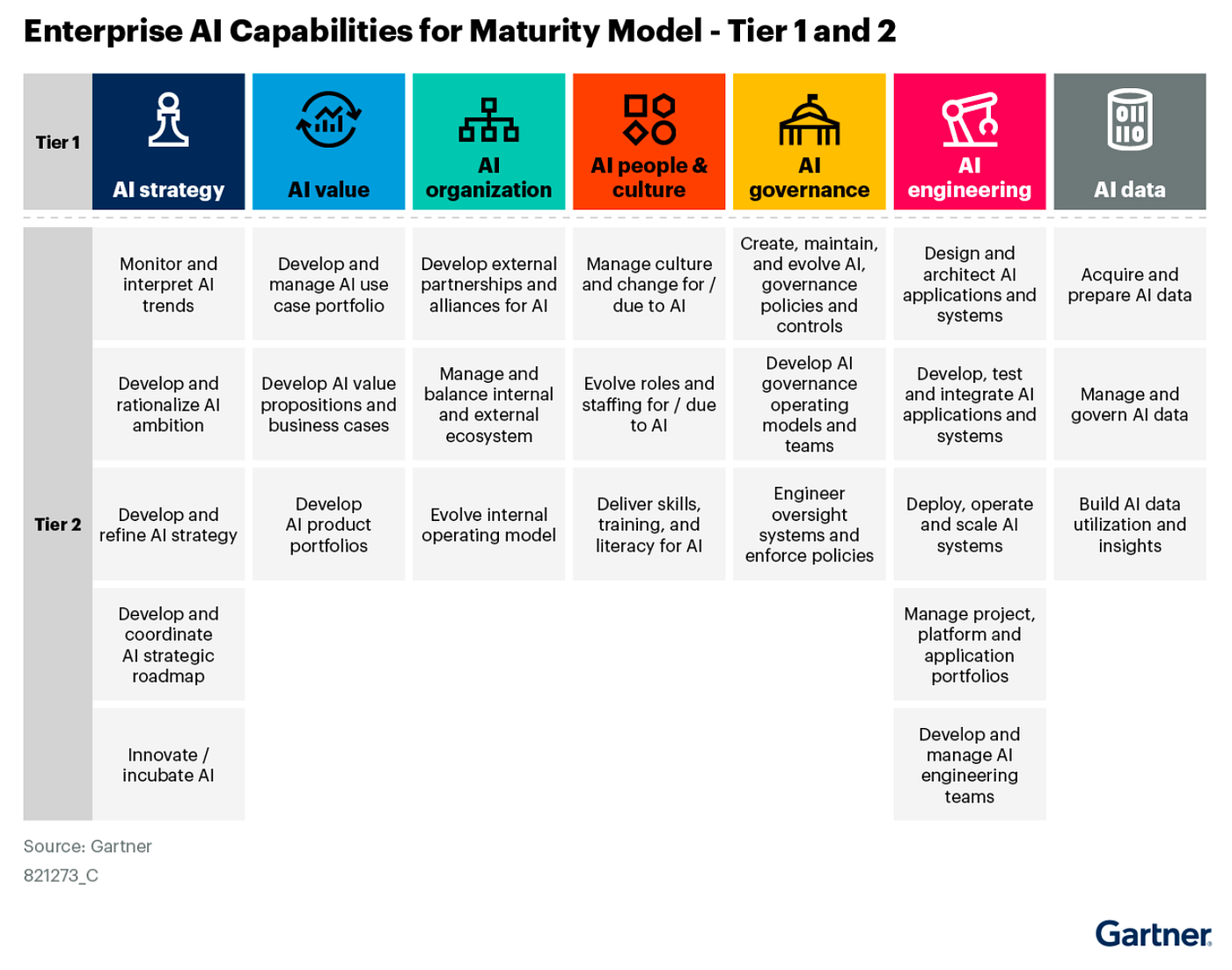

Understanding the Capability Tiers

The Gartner model organizes maturity into a hierarchy of capabilities.

Understanding the Capability Tiers

To apply this roadmap to banking, we must view the Gartner model’s tiers not just as abstract categories, but as operational domains. The model identifies seven high-level capabilities. In a banking context, these translate as follows:

- AI Strategy: Moving beyond “we need AI” to specific alignment with Retail, Wealth, or Institutional goals (e.g., “AI for Hyper-personalization in Wealth Management”).

- AI Value: The transition from vanity metrics to tangible P&L impact (e.g., reducing False Positives in AML checks).

- AI Organization: Evolving from a federated “Center of Excellence” to embedded AI product teams within lines of business.

- AI People & Culture: Shifting from “hiring data scientists” to upskilling the entire risk and compliance workforce on Generative AI.

- AI Governance: The bedrock of banking AI — ensuring Explainability (XAI), Fairness (Fair Lending), and Safety.

- AI Engineering: Modernizing the “plumbing” — integrating Python/PyTorch pipelines with COBOL/Mainframe cores.

- AI Data: Moving from data swamps to curated Feature Stores compliant with BCBS 239.

Tier 2 & 3: The Banking Capabilities

The model creates granularity through Tier 2 (Clusters) and Tier 3 (Specific Capabilities). Below is the translation of these generic concepts into specific financial services operations:

- Governance >> Risk Frameworks >> Model Risk Management. The General Capability could be to “Develop AI risk frameworks”. This capability focuses on integrating LLMs into existing Model Risk Management (MRM) policies. It assesses the institution’s ability to validate non-deterministic models against strict regulatory expectations for safety and soundness.

- Engineering >> Operate AI Systems >> MLOps & Lineage. The General Capability could be to “Operationalize AI systems”. This represents the maturity of MLOps (Machine Learning Operations). The critical test is whether the bank can retrain a credit scoring model, validate it, and deploy it to production without breaking the data lineage required for a regulatory audit trail.

- Data >> Manage AI Data >> Privacy & Security. The General Capability could be to “Assure security and privacy for AI data”. This refers to the technical capability to perform dynamic masking of PII within training datasets. It also entails strictly enforcing “Chinese Wall” policies to segregate investment and advisory data during the model training process.

Conducting the Assessment

How does a bank practically assess itself against these pillars? The assessment should not be a “tick-box” exercise but a strategic audit.

- Using a scoring tool, stakeholders must map their “Current Maturity” against their “Target Maturity”. It is acceptable to aim for Level 3 in HR systems while aiming for Level 5 in Fraud Detection.

- Do not let IT do this alone. The assessment requires input from Risk, Legal, Business Lines, and HR. If IT rates Data Maturity as a “4” but the Mortgage team rates it a “1” because they can’t access the data they need, that discrepancy is a critical finding.

- The “delta” between current and target states reveals the roadmap. If the gap in “AI Governance” is the largest, that becomes the Year 1 priority.

Maturity is not a destination; it is a continuous loop of assessment and improvement . Banks that remain stuck in Level 2 (Experimenting) risk becoming backend utilities for more agile Fintech competitors. By using the Assessment Tool provided in this kit, bank leaders can “meter and rationalize their ambition” , ensuring that their investment in AI yields safe, compliant, and profitable growth.

Achieving AI maturity is not an endpoint; it is a state of “continuous improvement”.

The “Adaptive Bank”

The ascent from Level 1 to Level 5 is not merely an upgrade in software; it represents the metamorphosis of a traditional financial institution into a technology company that holds a banking license. The “Adaptive Bank” of the future will transcend simple cost-saving measures, instead using AI to fundamentally reimagine the mechanics of value exchange, risk management, and the architecture of customer trust.

The necessary tools and frameworks are already in place. The competitive edge now lies entirely in the execution of the roadmap and the rigor of the transition’s governance.

As the chasm between “experimenting” and “leading” widens, the AI Maturity Model serves banking executives as both a mirror and a map. It provides the necessary structure to “meter and rationalize” ambition against current readiness, establishing a clear, evidenced-based “roadmap for development” .

The question is no longer if AI will transform the industry, but which banks possess the organizational maturity to harness that transformation. The winners will be those who stop treating AI as a siloed technology project and start building it as a total enterprise capability.

[Download the Banking AI Maturity Assessment Tool Here]