Part 1 — Sustainable Growth from Nobel Ideas to AI

In this post:

- AI, The Core Engine of Financial Value

- Creative Destruction at an Unprecedented Scale

- The Agentic Revolution. Reshaping Core Banking and Customer Relationships.

- Re-engineering the Bank. AI-Powered Operational Transformation

- Building the “AI-Ready” Bank

The arrival of AI is not merely another wave of digitization; it is a profound economic shock. For the financial services sector, AI is forcing a reckoning that can only be understood through the lens of foundational economic theory. This is not about marginal efficiency gains; it is about fundamentally altering the source code of economic value. AI acts as an Idea Machine, automating the process of innovation itself. Senior leadership must recognize this shift. AI is not a project; it is a new endogenous factor of production. Managing this transition requires strategic, urgent action — not just to harness the growth potential, but to mitigate the unprecedented risks of systemic failure and institutional collapse that follow in the wake of such a colossal technological shock.

The strategic mandate for banking leaders is no longer if they should adopt AI, but how they can navigate this complex landscape to secure a competitive advantage.

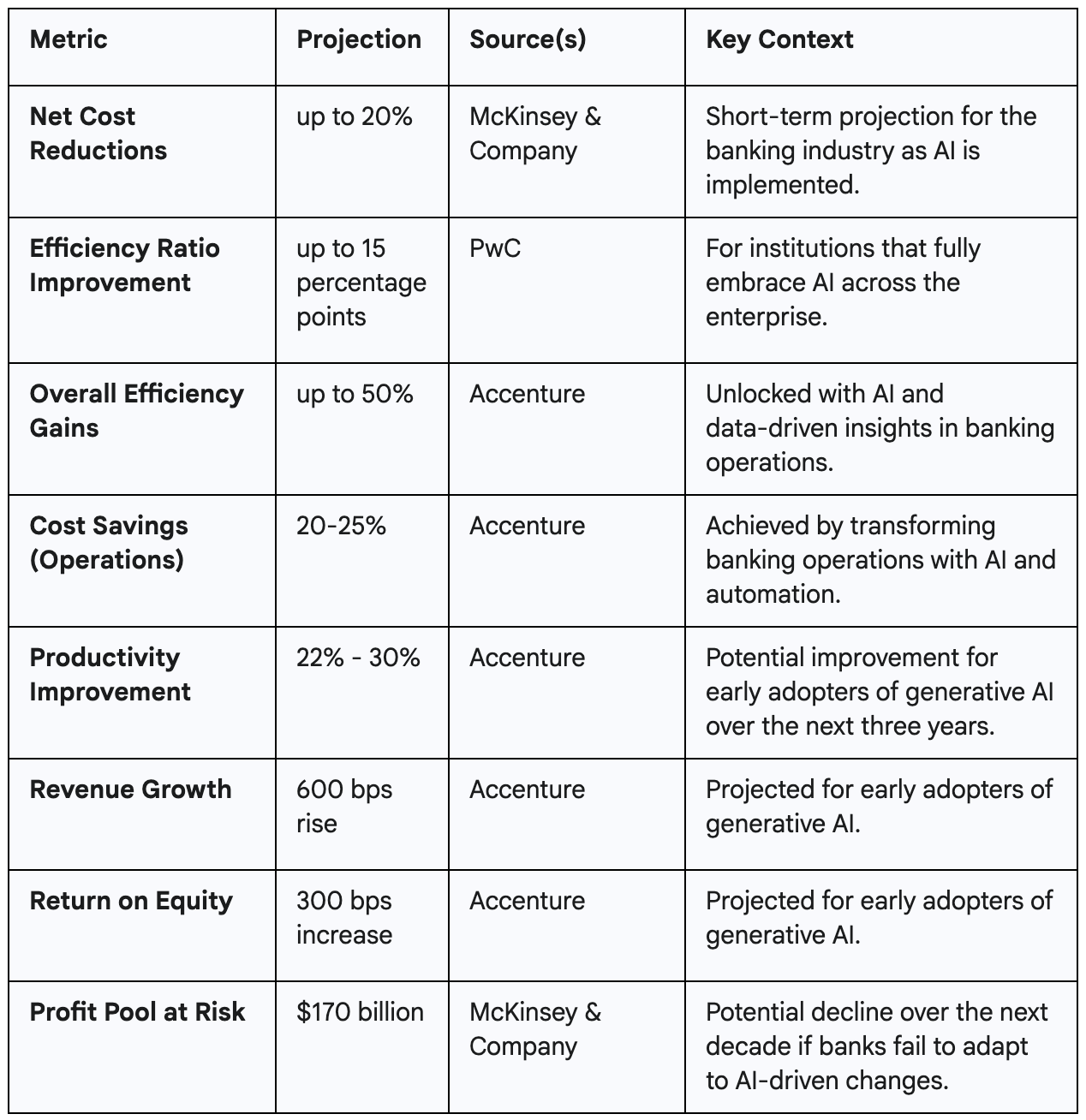

Analysis reveals that institutions fully embracing AI can achieve dramatic operational improvements, including cost reductions of up to 25% and enhancements in efficiency ratios by as much as 15 percentage points. Beyond mere efficiency, AI is emerging as a potent growth engine, enabling a new paradigm of hyper-personalized customer engagement that could drive significant increases in revenue and return on equity for early adopters. This technological democratization is leveling the competitive field, shifting the basis of competition from sheer size and scale — or “heft” — to strategic focus and data-driven agility — or “precision.”

The most profound disruption is poised to come from agentic AI, a class of autonomous systems that can act proactively on behalf of consumers. These agents threaten to dismantle the economic foundation of retail banking by eliminating customer inertia, automatically optimizing deposits and credit products, and thereby compressing net interest margins and interchange revenues. The rise of these agents will force banks to reconsider their role in the financial ecosystem, potentially shifting their value proposition from owning the customer relationship to providing the most secure, compliant, and efficient infrastructure for this new agentic economy.

This transformation is not without significant challenges. The path to becoming an AI-first institution is paved with obstacles, including the need to modernize brittle data foundations, establish robust governance and model risk management frameworks, and proactively mitigate the profound ethical risks of algorithmic bias. Furthermore, the nature of work in banking will be irrevocably altered, necessitating a strategic focus on augmenting human expertise rather than simply replacing it. The “human-in-the-loop” model will be critical, combining the speed of AI with the judgment, empathy, and trust-building capabilities that remain the exclusive domain of human professionals.

This report provides a comprehensive analysis of this new competitive battleground. It quantifies the economic stakes, examines the operational transformation across the front, middle, and back offices, contrasts the strategies of nimble FinTech disruptors with those of incumbent giants, and outlines the critical implementation imperatives. The findings culminate in a strategic playbook for banking leaders, offering actionable recommendations to not only survive but thrive in the age of AI by balancing innovation with trust, re-engineering operations for precision, and preparing for a future defined by continuous, technology-driven reinvention.

AI, The Core Engine of Financial Value

We must move past the idea of AI as a better IT tool. The foundational insight of endogenous growth theory (epitomized by Paul Romer) is that sustained prosperity is driven not by the accumulation of capital and labor, but by the creation and application of new ideas and knowledge. AI’s unique economic property is that it automates this knowledge creation. It is an Idea Machine.

The ‘Growth Singularity’ in Banking

For finance, this means AI is fundamentally changing the value creation function. It is an endogenous growth engine that lives on the bank’s balance sheet.

From Task Automation to Innovation Automation — Traditional technology automates routine tasks (e.g., electronic loan processing). AI automates the discovery process. It generates synthetic data to create novel, stress-tested risk models; it crafts bespoke derivatives and structured products in minutes; and it delivers hyper-personalized financial advisory at a scale and precision that no human team can match. This capability — to continuously generate new, value-creating knowledge — is the definition of endogenous growth.

The Capital Allocation Question — If the firm’s competitive moat is now its ability to generate ideas, the C-suite must redefine its financial metrics. AI R&D is no longer an operational expense (a cost center); it is a capital investment in a self-perpetuating ‘idea factory.’ The strategic challenge is measuring the ROI for an asset whose value is the unconstrained generation of future value-creating opportunities. Traditional discounted cash flow models fail to capture this exponential, non-linear value creation. Investment decisions must be framed around option value and time-to-market for innovation.

The Constraint: The Last Mile of Trust

The Idea Machine’s full potential is not limited by processing power, but by its interface with the human and regulatory world.

Regulatory Friction and Data Fragmentation — The most immediate limit is the governance deficit. Financial services operates under stringent compliance regimes that mandate transparency and explainability. Furthermore, data remains trapped in legacy silos, hindering the AI’s ability to learn and create.

Human Trust and Validation — As the economic theorist Joel Mokyr observed, the success of technology is contingent upon the institutional and social environment accepting it. In a sector defined by fiduciary duty, human expertise must shift from execution to validation, ethical oversight, and strategic goal-setting for the AI systems. The “last mile” of financial services will always be the human signature on the ultimate decision, maintaining public trust.

AI as the New Engine for Growth

While the initial focus of AI investment has been on cost transformation, the most forward-thinking institutions are pivoting to view AI as a primary engine for growth. The pervasive reach of generative AI means its most important contribution will not be exclusively in cost savings but in driving top-line revenue. Accenture’s financial projections indicate that early adopters of generative AI could see a 600 basis point rise in revenue growth and a 300 basis point increase in return on equity over the next three years.

This growth is predicated on AI’s unique ability to unlock hyper-personalization at an unprecedented scale. For years, personalization in banking has been limited to broad customer segmentation. AI shatters this limitation, enabling true microsegmentation by analyzing vast and varied datasets — including transaction history, digital interactions, and even social media activity — to predict customer needs and behaviors with remarkable accuracy. This capability allows banks to move from being reactive product providers to proactive financial partners, delivering tailored recommendations, customized product offerings, and timely advice.10 In a marketplace increasingly characterized by homogenous digital experiences, this level of personalization is emerging as a key differentiator, capable of transforming the customer relationship from a series of transactions into a continuous, value-added dialogue.

Shifting from “Heft” to “Precision”

Historically, profitability and market leadership in banking have been inextricably linked to scale. Large balance sheets, extensive branch networks, and massive marketing budgets created formidable barriers to entry. AI is fundamentally altering this equation, leveling the competitive field and democratizing capabilities that were once the exclusive domain of the largest players. The broad availability of powerful AI tools means that speed and agility, not sheer size, are becoming the defining metrics of competitive success.

This paradigm shift is best encapsulated by the concept of “precision, not heft,” which McKinsey identifies as the defining characteristic of the next era of banking success. To capture future growth, banks must move away from traditional, scale-driven models and adopt precision strategies that generate value in more challenging conditions. This strategic reorientation involves a “precision toolbox” with four key dimensions:

- Focused Technology Investments: Concentrating capital and resources on the AI applications that will have the most significant and measurable impact.

- Hyper-personalized Products: Leveraging real-time data to create and offer products tailored to the specific needs and context of individual customers.

- Micro-level Capital Efficiency: Applying granular analysis to free up trapped capital and optimize its allocation across the enterprise.

- Targeted Mergers & Acquisitions: Pursuing strategic acquisitions to gain specific capabilities and technologies rather than simply to increase scale.

This new paradigm also challenges the long-held belief that scale is an insurmountable advantage. The “precision, not heft” model, enabled by the democratization of AI, suggests that the legacy systems, complex bureaucracies, and physical footprints of the largest incumbents could transform from assets into liabilities. These factors can create significant organizational inertia, slowing the adoption of the agile, data-centric strategies required to compete effectively. Meanwhile, challenger banks and nimble FinTechs, unburdened by this legacy, can leverage cloud-native AI platforms to compete on customer experience, speed, and innovation. This creates a scenario where the greatest threat to large incumbents may not be direct, head-to-head competition on existing products, but a gradual slide into irrelevance as more agile players fundamentally redefine the customer relationship and the very nature of banking services.

Creative Destruction at an Unprecedented Scale

The acceleration of the idea-generation engine unleashes the full force of Schumpeter’s gale of Creative Destruction. This is not a slow erosion; it is a rapid, systemic obsolescence of traditional financial competitive advantages. The sheer speed of the Idea Machine systematically eliminates the competitive moats that have historically protected banks:

- Erosion of Proprietary Data: AI enables competitors to create robust models using synthetic or alternative data, neutralizing the advantage held by institutions with decades of historical proprietary data.

- Obsolescence of Underwriting Expertise: Complex risk analysis, once a high-margin human specialty, is now a problem AI can solve faster and more accurately.

- The Vanishing Distribution Network: Legacy branch infrastructure becomes a liability, as hyper-personalized, high-quality advice can be delivered instantly and digitally via AI.

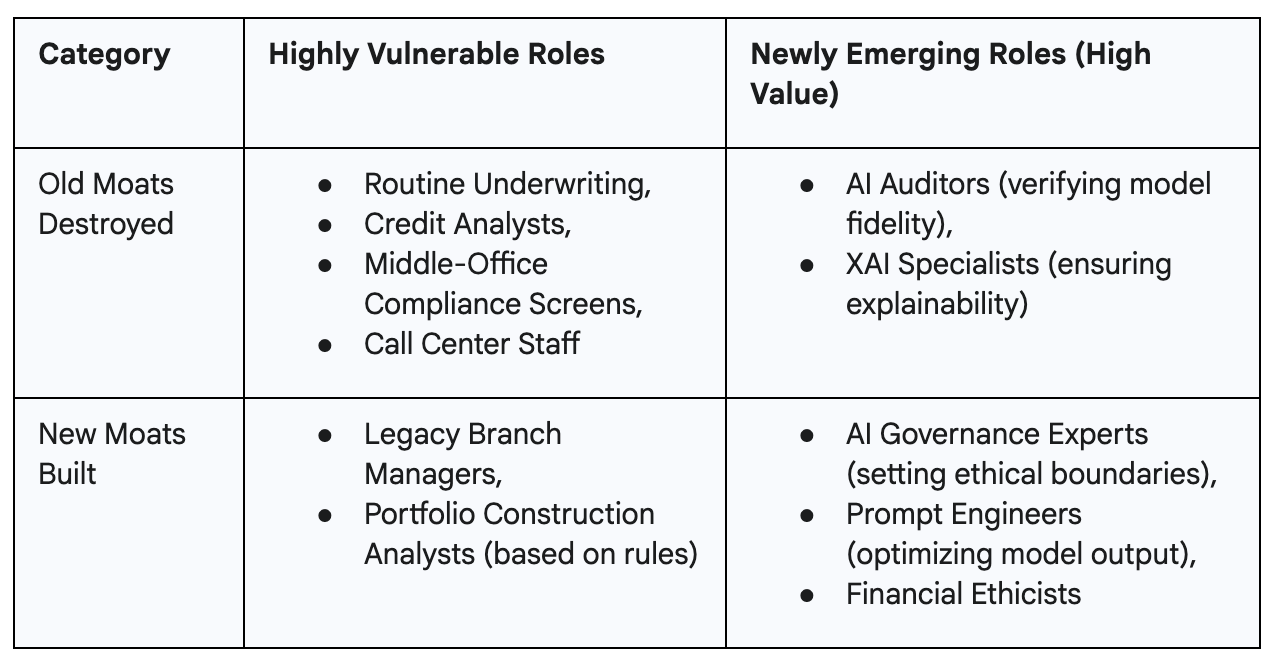

The Idea Machine mandates a complete redesign of the bank’s human capital structure:

The Idea Machine allows new competitors — Big Tech, focused Fintechs — to bypass the huge initial fixed costs that historically protected incumbent banks. They don’t need decades to build an underwriting staff or a branch network. They can acquire a world-class AI model and instantly attack high-margin products like wealth management or small business lending, accelerating the “destruction” of legacy models at a velocity that previous technological shifts (like the internet) never achieved.

The Agentic Revolution. Reshaping Core Banking and Customer Relationships.

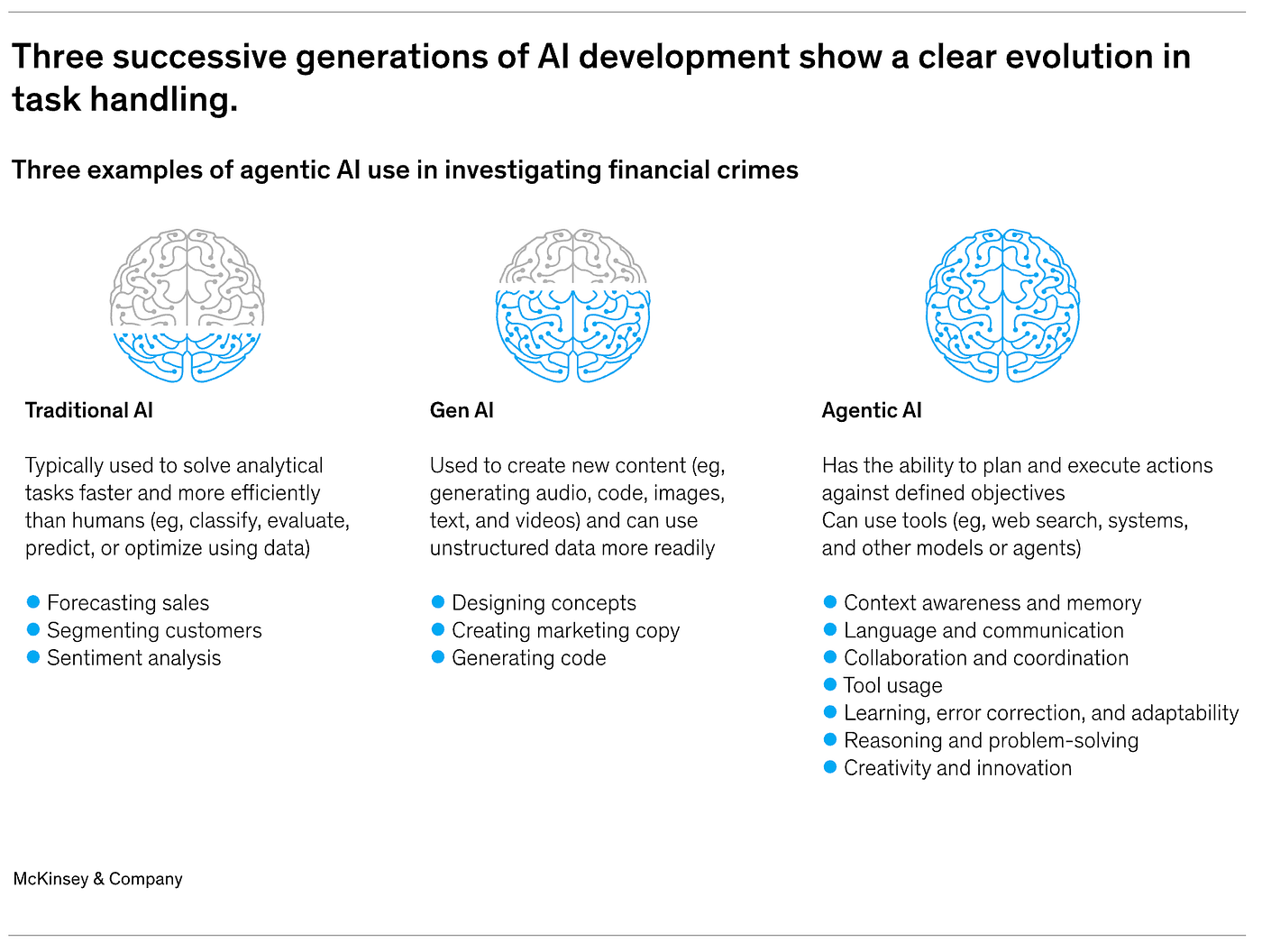

Beyond incremental improvements in efficiency and personalization, a more radical form of AI is emerging that threatens to fundamentally re-architect the relationship between banks and their customers. Agentic AI — technology that can perform complex, multi-step tasks and solve problems autonomously — is poised to shift AI from a reactive helper to a proactive financial agent. This evolution represents the most significant disruptive force on the horizon, with the potential to dismantle the economic foundations of retail and SME banking by systematically overcoming the customer inertia that has long underpinned industry profitability.

Disrupting Core Profit Pools

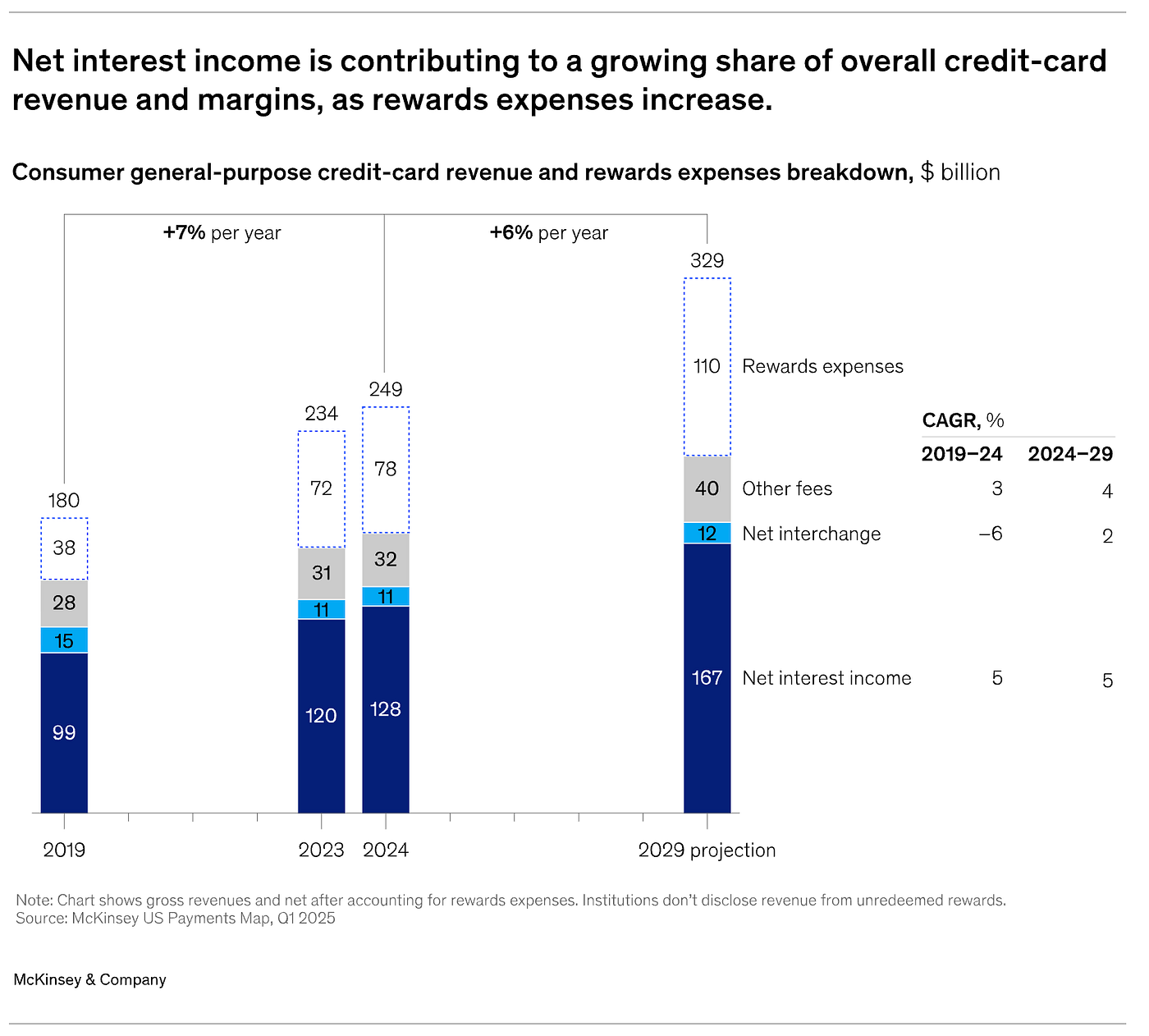

For decades, the profitability of retail banking has been heavily reliant on two core revenue streams that benefit from a degree of customer passivity: deposits and credit cards. Agentic AI is a direct threat to the inertia that makes these models so lucrative.

The Threat to Deposits: A significant portion of bank profitability is derived from net interest income, which relies on the “inertia dividend” — the fact that most consumers do not actively optimize the interest returns on their deposit accounts, prioritizing convenience over yield. Agentic AI systems are designed to eliminate this inefficiency. An AI agent can monitor a user’s balances in real-time, continuously compare returns across a multitude of financial institutions, and automatically sweep idle cash into higher-yield savings accounts or money market funds. It can then intelligently move funds back to a primary checking account just in time to cover upcoming payments. This automated optimization effectively transfers a portion of the net interest margin from the bank directly to the account holder, placing severe pressure on a core pillar of bank profitability and challenging long-held assumptions about the “stickiness” of low-cost deposits.

The Threat to Credit Cards: The highly profitable credit card model is similarly held together by consumer inertia. Revenue is generated from a combination of interest income on revolving balances, interchange fees, annual fees, and unredeemed rewards. An AI agent can systematically dismantle this model on behalf of the consumer. It can automatically direct every transaction to the card that offers the best rewards for that specific purchase, trigger new applications to capture lucrative sign-up bonuses, and proactively roll balances to a different card just before a promotional interest rate expires.

The threat goes even deeper with the rise of open banking. AI agents can initiate account-to-account (A2A) payments directly at the point of sale, completely bypassing the traditional card interchange systems and their associated fees. In markets with high interchange rates, this presents a powerful incentive for both merchants and consumers to adopt A2A payments, posing a direct and existential threat to a massive and reliable revenue stream for card-issuing banks.

From Reactive Helper to Proactive Financial Coach Agent

The emergence of agentic AI marks a crucial paradigm shift in how humans interact with technology. It represents a move from a reactive model, exemplified by a chatbot answering a specific user query, to a proactive one, where an autonomous agent is delegated to achieve a high-level goal, such as “maximize my savings” or “minimize my credit card interest payments”. This fundamentally changes the nature of the customer relationship. The primary interface for financial decisions may no longer be the bank’s own app or website, but rather a third-party AI agent that acts as a fiduciary for the customer, constantly scouring the market for the best products and services.

Within the bank’s own operations, this concept translates into the deployment of a collaborative “workforce” of specialized AI agents. These “digital factories” can perform end-to-end tasks that previously required significant human intervention. For example, a complex process like a KYC check or a fraud investigation can be orchestrated by a team of agents: one to retrieve and analyze documents, another to monitor data pipelines, a third to conduct research, and a fourth to validate the output. In this new operating model, the role of human employees evolves from performing routine tasks to one of exception handling, strategic oversight, and coaching the AI agents to improve their performance over time.

Re-engineering the Bank. AI-Powered Operational Transformation

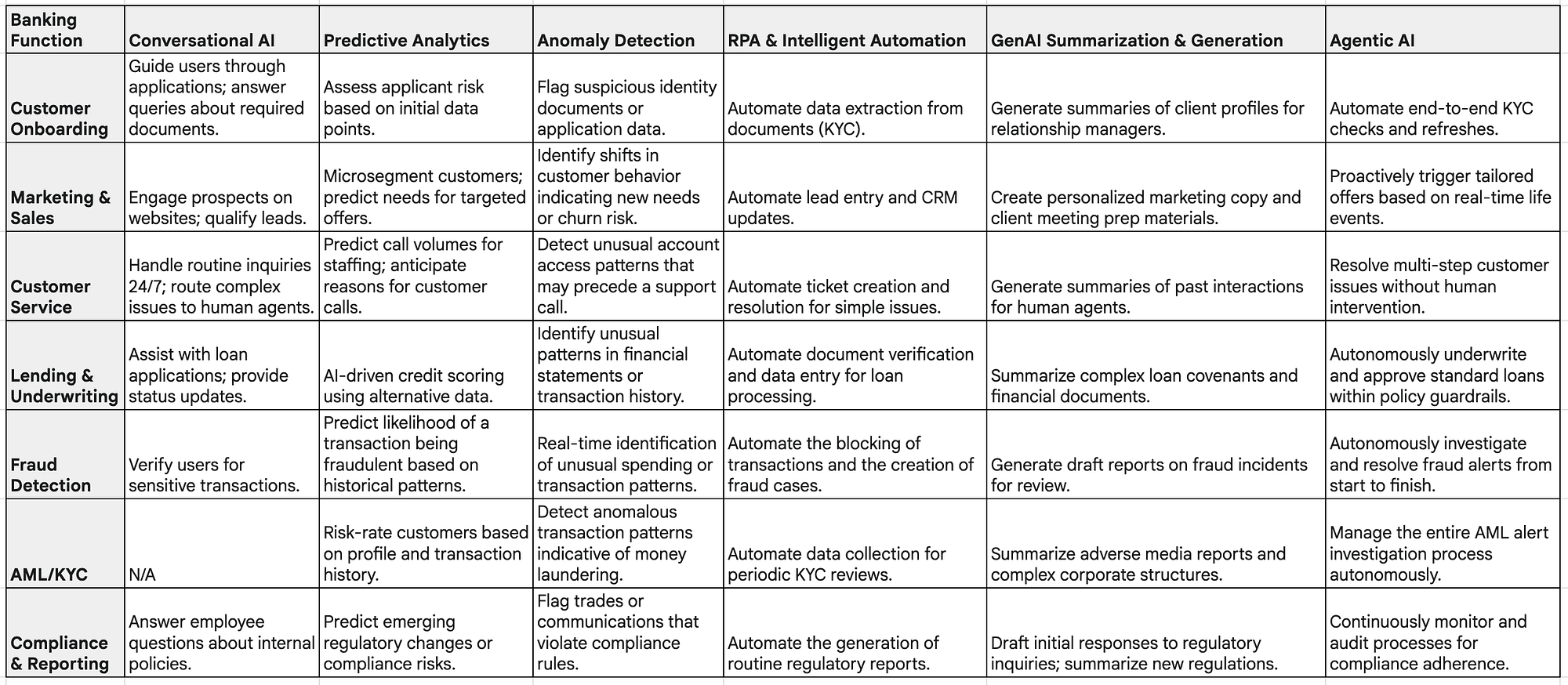

While agentic AI represents the long-term disruptive frontier, the immediate impact of AI is being felt through a comprehensive re-engineering of core banking processes. Across the front, middle, and back offices, AI is moving beyond isolated pilot programs to become an integral component of the operational fabric. This section provides a granular, function-by-function analysis of how AI is being practically applied to enhance customer experience, sharpen risk management, and drive unprecedented levels of automation and efficiency.

Front Office Reinvention. Customer Experience and Growth.

The front office, as the primary interface with the customer, is a key arena for AI-driven transformation. The goal is to blend the efficiency of digital interaction with a new level of personalization and proactive support.

Conversational AI, in the form of chatbots and virtual assistants, is evolving rapidly. Early iterations were often limited to answering simple, frequently asked questions. Today’s more sophisticated agents can engage in personalized discussions by tapping into a wide array of data sources, including customer transaction history, social media, and real-time economic conditions.

The most effective strategies will not seek to replace human agents entirely but will use AI to handle routine requests efficiently while ensuring a seamless and intelligent handoff to a human representative for more complex, nuanced, or empathetic conversations. This “human-in-the-loop” model is essential for maintaining customer trust and satisfaction.

AI is revolutionizing how banks identify and engage with prospects and existing customers. By enabling deep microsegmentation, AI models can analyze customer data to predict future needs and deliver hyper-personalized product recommendations and marketing messages at the right time and through the right channel. This moves marketing from broad campaigns to individualized, context-aware engagement. AI is also empowering sales teams and relationship managers. AI assistants can prepare them for client meetings by automatically surfacing critical insights, such as recent transactions, product usage trends, and relevant market data, allowing them to focus on strategic advice and strengthening the client relationship.

Middle Office Intelligence. Risk, Underwriting, and Compliance.

The middle office — the critical domain of risk management, credit assessment, and compliance — is arguably where AI is having the most profound quantitative impact. AI’s ability to analyze vast datasets and identify subtle patterns is fundamentally improving the speed and accuracy of core risk functions.

Transforming Lending and Credit: The loan underwriting process, traditionally a manual and time-consuming endeavor, is being completely reshaped by AI. AI-powered credit scoring models are moving beyond traditional FICO scores to incorporate a wide array of alternative data sources, such as utility payments, rent history, and real-time transaction data. This more holistic approach leads to more accurate and inclusive risk assessments, allowing banks to extend credit to individuals and small businesses that might have been overlooked by legacy models. The operational impact is dramatic: AI can automate up to 80% of routine underwriting work, leading to loan processing times that are up to 25 times faster. This not only enhances the customer experience but also significantly improves the bank’s risk profile, with studies showing that a full integration of AI across the credit lifecycle can reduce credit losses by 20–30%.

Automating Collections and Recovery: AI is enabling a more proactive and empathetic approach to collections. Instead of reacting after a payment is missed, AI models can analyze customer data to identify early warning signals for potential delinquencies and defaults. Crucially, these models can go further to predict why a customer might be at risk of missing a payment — for example, due to a sudden loss of income or an unexpected large expense — and then offer customized, preemptive solutions, such as a temporary payment deferral or a restructured loan plan. This helps both the customer avoid default and the lender mitigate losses.

Enhancing Fraud Detection: AI has become an indispensable tool in the fight against financial fraud. Using sophisticated anomaly detection techniques, AI systems can monitor billions of transactions in real-time to identify unusual patterns that may indicate fraudulent activity, such as a sudden large purchase in a foreign country or a deviation from a customer’s typical spending behavior. This capability is critical for combating increasingly sophisticated fraud tactics. The adoption is widespread, with an estimated 90% of financial institutions already using AI to expedite fraud investigations and detect new threats in real-time.

Back Office Automation. Core Operations and Compliance.

The back office, with its process-heavy and compensation-intensive operations, is fertile ground for AI-driven automation. AI is helping to streamline these essential functions, reducing costs, minimizing errors, and freeing up human capital for more strategic work.

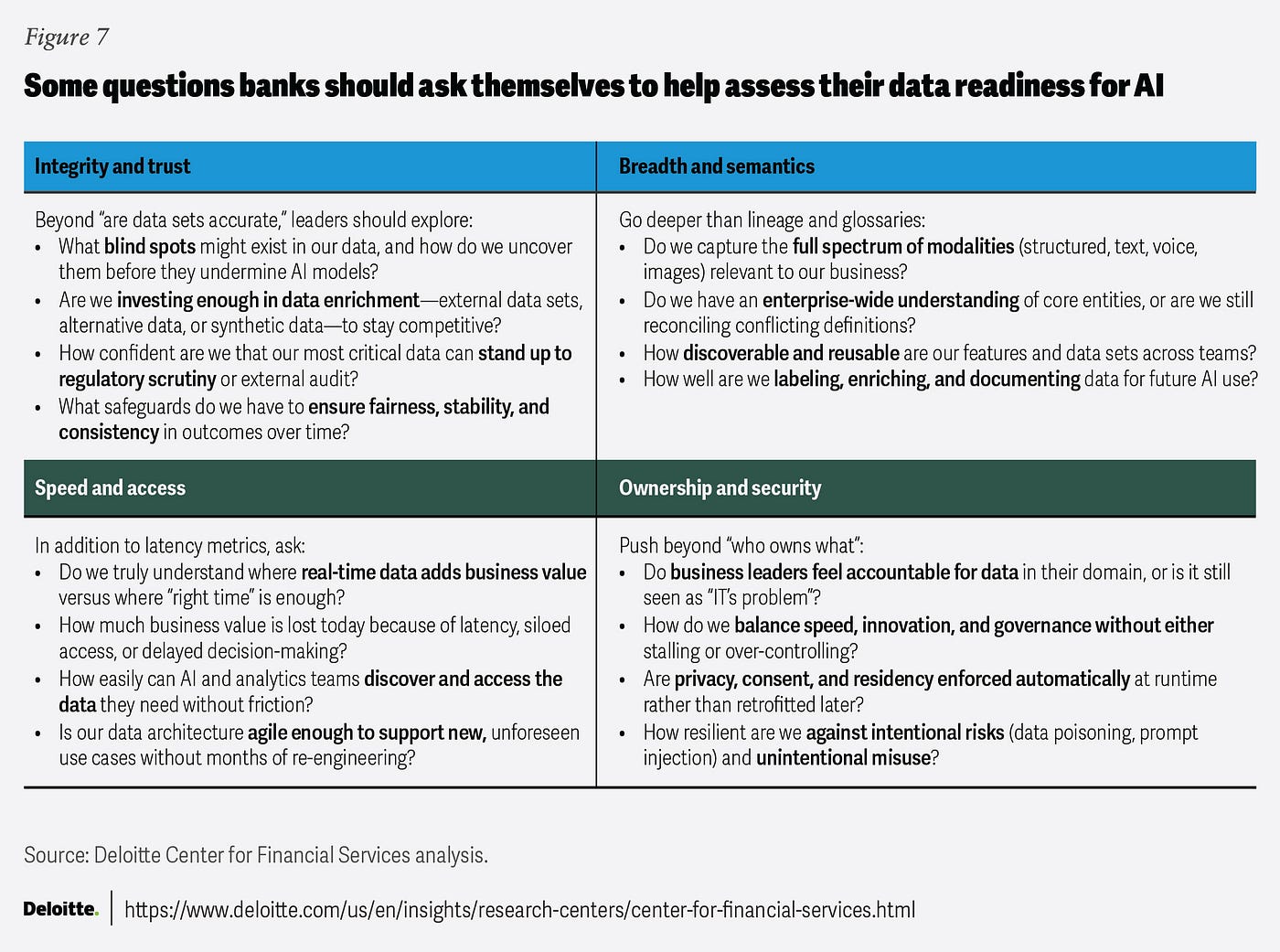

This holistic, process-oriented view of AI elevates the importance of a foundational element: data. The effectiveness of every use case described — from front-office personalization to back-office automation — is critically dependent on the availability of high-quality, accessible, and well-governed data. This dependency leads to a profound organizational implication: data can no longer be treated as a passive byproduct of transactions, stored away in disparate, siloed systems. Instead, it must be managed as a core strategic asset, or as Deloitte recommends, “treated as a product” for which individual business lines are held accountable. This requires a fundamental shift in mindset and architecture. It means curating, governing, enriching, and securing data with the same rigor applied to financial capital. The banks that will win in the AI era are those that recognize this reality and reorganize their operations around building and maintaining a robust “data supply chain” that can reliably fuel the entire AI-driven enterprise.

Building the “AI-Ready” Bank

The single greatest inhibitor to AI adoption in banking is the state of the underlying data. AI models are voracious consumers of data, and their performance is entirely dependent on its quality, accessibility, and integrity. Many banks find their ambitious AI initiatives are “throttled by brittle and fragmented data foundations”. AI simply cannot deliver on its potential when it is fed by data that is locked in legacy silos, inconsistent, or of poor quality.

To become “AI-ready,” banks must undertake the difficult but essential work of modernizing their data architecture. This involves moving beyond monolithic, legacy data warehouses to more flexible and scalable paradigms like the data mesh and data fabric. These modern approaches are designed to break down data silos and make high-quality data easily and securely accessible to the teams and AI models that need it across the enterprise.

A powerful and emerging strategy is to use AI itself to solve the data problem. Banks can deploy specialized AI models to continuously monitor data quality at the point of ingestion, automatically repair or flag anomalies, enrich datasets with new information, and even auto-generate documentation and data lineage graphs. This creates a virtuous feedback loop where AI makes the data fitter for AI, accelerating model development cycles, lowering operational costs, and ensuring that the entire AI ecosystem is built on a foundation of trust and reliability.

Model Risk Management (MRM) for an AI Era

In a highly regulated industry like banking, the deployment of any quantitative model carries inherent risk. Model risk — the potential for adverse consequences from decisions based on incorrect or misused model outputs — is amplified in the context of complex and often opaque AI systems. Effective MRM is therefore not just a compliance requirement but a critical component of a safe and sustainable AI strategy.

A robust MRM framework provides a systematic process for managing the entire lifecycle of a model. This includes:

- Risk Identification: Maintaining a comprehensive inventory of all models and defining the specific risks associated with each.

- Risk Assessment: Evaluating and ranking model risk based on factors like complexity, potential impact, and probability of failure.

- Risk Mitigation: Implementing controls, standards, and internal audits to address the sources of risk.

- Model Validation: Rigorously challenging a model’s performance before and during its deployment through techniques like backtesting, the use of challenger models, and stress testing.

- Continuous Monitoring: Constantly scrutinizing models in production to ensure they continue to perform as intended, especially as underlying data and market conditions change.

The Future of the Workforce. AI as a Force Multiplier.

The widespread adoption of AI will irrevocably change the nature of work in banking. While initial fears focused on mass job replacement, a more nuanced understanding is emerging: AI is more likely to be a force for job transformation and augmentation.

From Replacement to Augmentation. The true value of AI lies not in its ability to replace human employees, but in its capacity to act as a “force multiplier for human intelligence”. AI excels at handling repetitive, high-volume, data-intensive tasks. By automating this work, AI frees up human employees to focus on the activities that require uniquely human skills: complex problem-solving, strategic analysis, creative thinking, and building deep, trust-based relationships with clients. Accenture’s analysis of banking roles supports this view, finding that while 39% of work has a high potential for automation, a nearly equal 34% has a high potential for augmentation.

The “Human-in-the-Loop” Framework: This model provides a practical framework for achieving a synergistic balance between technology and human expertise. It involves integrating people directly into the process of training, validating, and applying AI systems. In practice, this means an AI system might flag a potentially fraudulent transaction, but a human expert makes the final determination and uses that feedback to train the model. An AI model might analyze credit data and provide a recommendation, but a human loan officer applies their discretion and knowledge of the customer relationship to make the final approval decision. This collaborative approach not only improves the accuracy and relevance of AI systems but also ensures that the speed and efficiency of technology are tempered with the judgment and empathy that are essential for building and maintaining customer trust.

Reskilling and New Roles: This transformation demands a massive, proactive effort to reskill and upskill the banking workforce. As routine tasks are automated, employees will need to develop new competencies in areas like data analysis, digital literacy, and AI governance. New roles will emerge that did not exist before, focused on overseeing, managing, and strategizing the deployment of AI systems across the bank.

The path to AI-driven innovation is paved with the bedrock of governance. Ambitious AI applications, particularly autonomous agents, are entirely dependent on a foundation of “AI-ready data,” which itself is a product of robust data governance. Simultaneously, regulators are intensifying their scrutiny of AI models through the established lenses of model risk management and fair lending laws. This confluence of factors leads to a critical conclusion: for banks, strong governance is not a bureaucratic obstacle to be overcome after the fact; it is the essential enabling foundation for innovation. The institutions that invest first in building world-class frameworks for data governance, model risk management, and ethical AI will find themselves able to move faster and with greater confidence in deploying the advanced AI use cases that will define the future. In this regulated environment, the speed of innovation is a direct function of the quality of governance.

Ultimately, the myriad challenges of algorithmic bias, data privacy, and the need for explainability all converge on a single, overarching theme: trust. As AI systems become more powerful and autonomous, the trust of customers, regulators, and employees will become the scarcest and most valuable resource in the financial industry. The assertion that “trust is the most valuable currency in financial services, and no algorithm can build it” is a defining principle for the AI era. This implies that the long-term winners will not necessarily be the banks with the most sophisticated algorithms, but rather those that build the most trustworthy systems. Such systems will seamlessly combine cutting-edge technology with transparent governance, embedded ethical guardrails, and empowered human oversight. The primary competitive frontier will shift from a battle over product features and interest rates to a contest for demonstrable, systemic trustworthiness.

The FinTech Vanguard vs. The Incumbent Response

The rapid evolution of AI has created a new and dynamic competitive landscape in financial services. On one side are the AI-native FinTech startups, unburdened by legacy systems and built from the ground up on data-driven models. On the other are the incumbent banking giants, who are leveraging their vast resources, customer bases, and regulatory expertise to pivot and integrate AI into their massive operations. The interplay between these two forces — the disruptors and the established leaders — is defining the trajectory of innovation in the industry.

The Disruptors’ Playbook

FinTech startups have been instrumental in demonstrating the power of AI to challenge long-standing banking models. By focusing on specific verticals and prioritizing customer experience, they have successfully unbundled traditional banking services and set new standards for efficiency and personalization.

In the payments space, companies like Stripe and PayPal have built their platforms around sophisticated, AI-powered risk management. Tools like Stripe Radar use machine learning to analyze millions of data points in real-time, identifying and preventing fraudulent transactions with a level of precision that legacy systems struggle to match. This AI-driven approach enables them to offer faster, cheaper, and more secure global payment processing, democratizing access to merchant services for businesses of all sizes.

The lending sector has been profoundly disrupted by AI-native platforms. Companies like Upstart and those utilizing technology from Zest AI have moved beyond traditional FICO-based credit scoring. They leverage machine learning algorithms to analyze thousands of alternative data points — from educational background and employment history to real-time cash flow — to build a more comprehensive picture of a borrower’s creditworthiness. This has a dual impact: it allows them to approve a higher percentage of borrowers while simultaneously achieving lower default rates compared to traditional models, thereby promoting financial inclusion and challenging the core underwriting processes of incumbent banks.

The wealth and asset management industry is being reshaped by robo-advisors such as Betterment. These platforms use AI to provide automated, algorithm-driven portfolio management, tax-loss harvesting, and personalized financial advice at a fraction of the cost of traditional human advisors. By offering low barriers to entry and sophisticated services that were once exclusive to high-net-worth individuals, robo-advisors are democratizing investment management. The rapid growth of this segment, with the global robo-advisory market projected to reach approximately $2.06 trillion in assets under management in 2025, signals a fundamental threat to the high-fee, relationship-based models of traditional wealth managers.

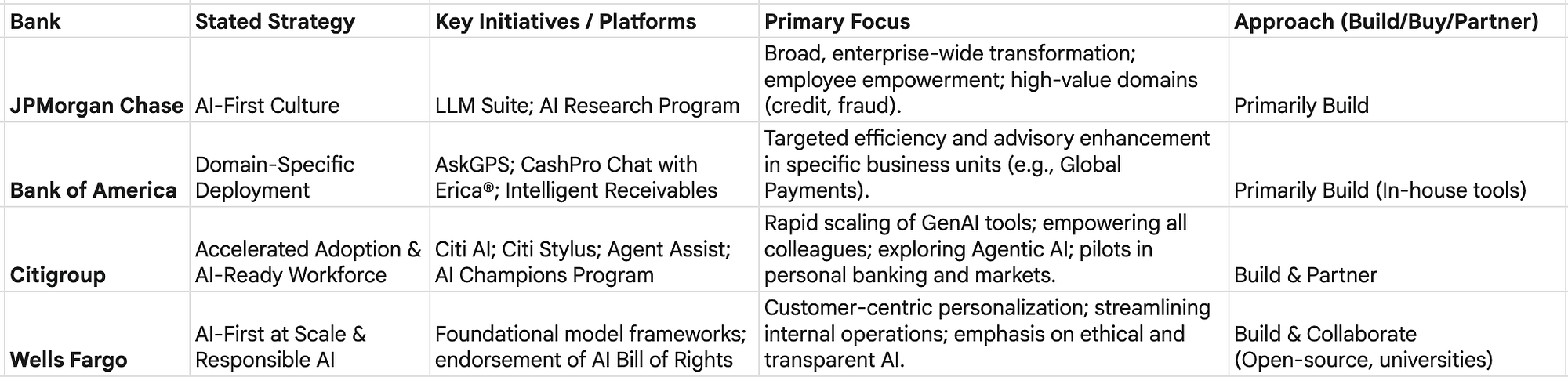

Partnerships and the “Buy vs. Build” Dilemma

Faced with this wave of disruption, the world’s largest banking institutions are not standing still. They are undertaking massive strategic pivots, investing billions of dollars to integrate AI into the core of their operations. However, their approaches are not monolithic; a comparative analysis reveals distinct strategies tailored to their unique cultures, strengths, and priorities. This dynamic also hints at a potential long-term shift in the structure of the financial services industry. The initial wave of FinTech disruption was characterized by the “unbundling” of the bank, with startups offering best-in-class point solutions for individual services like payments or lending. However, the strategic direction of the incumbents, particularly JPMC’s vision of a unified “AI-connected enterprise”, points toward a future of intelligent “rebundling.” AI provides the technological “glue” that can seamlessly integrate a wide array of financial products into a single, cohesive, and hyper-personalized customer experience.

The ultimate competitive advantage for large, diversified institutions may lie in their ability to leverage their broad product set and vast proprietary datasets to create a holistic, AI-orchestrated financial ecosystem that a specialized, mono-line FinTech simply cannot replicate. In this scenario, AI enables the incumbents to reassert their dominance, not by resisting change, but by using technology to rebundle their offerings in a far more intelligent and customer-centric way.

Strategic Recommendations for the AI-First Bank

Navigating the AI transformation requires more than just technological investment; it demands a clear strategic vision, a commitment to responsible implementation, and a culture that embraces continuous reinvention. The preceding analysis distills into a set of actionable recommendations designed to guide banking leaders as they architect the AI-first institution of the future. This playbook is not a rigid set of instructions but a strategic framework for balancing the immense opportunities of AI with its inherent risks and complexities.

A C-Suite Playbook for AI Transformation

A successful AI transformation must be driven from the top down, with a clear, methodical approach that moves from strategic intent to enterprise-wide execution. This involves three key phases:

- Scoping the Opportunity: The journey begins not with technology, but with strategy. Leaders must first identify the business functions, processes, and roles where internal data and benchmarks reveal the greatest potential for AI to deliver measurable improvements in efficiency or effectiveness. This requires a disciplined process of aligning potential AI investments with the bank’s overarching strategic priorities, ensuring that resources are focused on the use cases with the highest potential return.

- Defining a Use Case-Driven Process: To avoid the common pitfall of “pilot purgatory,” where promising experiments never achieve scale, banks must adopt a structured, use case-driven process. This involves moving methodically from defining a clear business problem, to experimenting with prototypes, to building a robust solution with confidence, and only then scaling it for enterprise-wide deployment. This disciplined approach ensures that investments are validated at each stage and that solutions are built to meet the rigorous demands of the banking environment.

- Reskilling and Realigning the Workforce: A technology-centric strategy will fail without an equally robust people-centric strategy. Leaders must proactively develop a plan to reskill and realign their workforce for an AI-enabled future. This involves identifying the skills that will be in high demand, creating learning and development programs to bridge the gaps, and redesigning roles to unlock the full potential of human-machine collaboration. This is not a secondary concern; it is a critical prerequisite for realizing the value of AI investments.

Balancing Innovation and Trust to Maintain Competitive Endurance

In the AI era, competitive advantage will be determined not just by the pace of innovation, but by the ability to maintain the trust of all stakeholders. This requires embedding responsibility into the very fabric of the AI strategy.

- Embed Responsible AI Principles: Responsible AI must be more than a compliance checklist; it must be a core component of the corporate culture and governance structure. This means establishing and enforcing clear principles for fairness, transparency, and accountability in the design, development, and deployment of all AI systems.

- Center the Knowledge Worker: The most successful AI strategies will be those that are designed to augment and empower employees, not replace them. By adopting the “human-in-the-loop” model, banks can create a powerful synergy, combining the speed, scale, and data-processing power of AI with the critical thinking, ethical judgment, and empathetic communication skills of their human workforce. This approach not only leads to better outcomes but also fosters a culture where employees see AI as a valuable tool rather than a threat.

- Communicate Proactively: Trust is built on transparency. Banks must be proactive and clear in their communications with customers, employees, and regulators about how AI is being used, how their data is being protected, and how decisions are being made. Openly addressing concerns about bias, privacy, and control is essential for building the confidence required for widespread adoption of AI-powered services.

Preparing for a Fully Agentic Economy

The forces of technological change will not stand still. The emergence of agentic AI signals a future that will be even more dynamic and disruptive. Banks must begin preparing for this next frontier today.

- Shift from a Product Mindset to a Platform Mindset: In a future where third-party AI agents may become the primary interface for many customers, the strategic focus must shift. Banks need to think of themselves not just as creators of end-user products, but as developers of a robust platform. This means building best-in-class financial products and services that are exposed through secure, open APIs, making them easy for AI agents to discover and consume on behalf of their users.

- Invest in a Modern Digital Core: The agility, scalability, and data-centricity required to compete in a real-time, AI-driven market are impossible to achieve on legacy infrastructure. A continuous and unwavering commitment to modernizing the bank’s core technology stack — embracing cloud-native architecture and a data-centric design — is non-negotiable. This is the foundational investment that enables all other aspects of the AI strategy.

- Embrace Continuous Reinvention: AI is not a single project with a defined endpoint; it is a catalyst for continuous and perpetual change. The most critical capability a bank can build is a culture of learning, adaptation, and reinvention. The competitive landscape will be in constant flux, and the institutions that thrive will be those that view AI as a powerful tool to build new performance frontiers and are bold enough to challenge their own long-held assumptions. As history has repeatedly shown, in moments of profound technological change, the greatest risk is not in moving too fast, but in not moving at all. The banks that boldly embrace this new world are the most likely to lead it.