On this post:

- Executive Summary

- The Problem Nobody Talks About

- The Proof: Who’s Already Building the Octopus?

- The Architecture of Five Layers, One Closed Loop (5 Zones)

- The Coach — A Technical Deep Dive Into Empathy at Scale

- The Neuroscience of Financial Habit Formation

- The Three-Mesh Architecture

- What a “Segment of One” Actually Looks Like

- Signals That Feed the Meshes

- What Nobody Wants to Talk About

- The Build vs. Buy Reality

- The Cultural Vault

- The 90-Day Thin Slice

- For the Chief AI Officer: The End of the Model Zoo

- For the Chief Data Officer: The Signal Is the Strategy

- For the CEO: The Platform That Sells Itself

- For the Head of Retail: Your Monday Morning Just Changed

- The Only Architecture Where Everyone Wins

There’s a moment in Peter Godfrey-Smith’s Other Minds where he describes how the octopus processes information. Unlike us — with our centralized brains issuing commands down a spinal highway — the octopus distributes intelligence across its arms. Each arm has its own neural cluster. Each arm can taste, touch, and decide independently. The central brain sets intent. The arms execute with local autonomy.

For two decades, banking technology has been built on the human nervous system model: a central brain (core banking), a spinal cord (middleware), and dumb limbs (channels) that do exactly what they’re told. The data warehouse sits in a vault. The analytics team runs queries. A report gets emailed to an executive. The executive makes a decision. Someone files a Jira ticket. Engineering builds something. Six months later, the customer sees a slightly different banner.

That architecture is dead. Not dying — dead. The banks that understand this will own the next decade. The ones that don’t will spend $200 million on “AI transformation” and end up with a chatbot that tells customers their balance.

What I’m going to describe in this article is something we’ve been building at Backbase — not as a feature, not as a product bolt-on, but as an entirely new layer of the Banking operating model. We call it the Intelligence Layer. It is, architecturally, the octopus: distributed intelligence with coordinated intent.

But I want to be honest about something upfront. Designing this architecture was the easy part. The hard part — the part that determines whether any of this actually works — is the friction. Regulatory friction. Cultural friction. Data friction. Execution friction. I’ll address the architecture first, because you need to understand what’s possible before you can navigate what’s difficult. But the friction sections are the ones I’d urge you to read most carefully, because those are the sections that determine whether this lands in production or dies in a slide deck.

Executive Summary

For two decades, banking technology has relied on a centralized core communicating with “dumb” channels. That architecture is dead. Today’s expensive “AI transformations” typically yield just two things: inert dashboards for executives and glorified FAQ chatbots for customers. Neither creates a competitive moat. Neither generates revenue.

The banks that will dominate the next decade are adopting a new model: The Intelligence Layer. Architecturally, it functions like an octopus — distributed intelligence across all customer touchpoints, coordinated by a central strategic intent. It sits above your heavy legacy core (requiring no 5-to-10-year rip-and-replace) and closes the critical gap between insight and real-time action.

This playbook is a definitive, architectural guide for the C-suite to transition from transactional banking to cognitive banking. Inside, you will find:

- The Neuroscience of Banking: How agentic AI and Digital Twins deliver “empathy at scale,” turning raw data into proactive financial coaching that automatically drives product origination.

- Navigating the Friction: Pragmatic solutions to the hurdles that kill digital transformation. Learn how to satisfy regulators with Explainable AI (solving the “Black Box”), unite traditional relationship managers with data scientists, and navigate the “Build vs. Buy” dilemma.

- The 90-Day Thin Slice: A tactical roadmap to deploy a single commercial experiment, prove concrete ROI in three months, and scale based on actual P&L impact, not hype.

Whether you are the CEO, CRO, CDO, or Head of Retail, your specific blueprint is in this document. Stop buying disconnected ML models. Start building a proactive revenue engine.

The Problem Nobody Talks About

Here’s the dirty secret of banking AI in 2026: the industry has split into two halves that don’t talk to each other.

Half one built dashboards for executives. Beautiful, expensive, utterly inert. A Chief Retail Officer opens a Tableau dashboard, sees that churn is up 2.3% in the 25–34 segment, nods thoughtfully, and then… what? Calls a meeting. Assigns a task. Waits for the campaign team. Reviews creative. Approves. Deploys. By the time the response reaches the customer, 4,000 of them have already moved their savings to the competitor who triggered the churn in the first place.

Half two built chatbots for customers. “Hi! I’m your AI banking assistant! How can I help you today?” The customer types “check my balance.” The chatbot returns the balance. The customer closes the app. Revenue impact: zero. The chatbot is a talking ATM with better grammar.

Neither half is intelligence. A dashboard that can’t act is a museum exhibit. A chatbot that can’t think is a phone tree with better grammar. Intelligence is the connection between knowing and doing — and in banking, that connection has never existed.

Until now.

But before I describe the architecture, let me show you what it looks like when someone gets this right.

The Proof: Who’s Already Building the Octopus?

DBS Bank in Singapore didn’t set out to build an “Intelligence Layer.” They set out to become a technology company that happens to have a banking license. By 2023, they had deployed over 300 AI/ML models in production — not in a lab, not in a pilot, in production. Their “Customer Science” team doesn’t report to IT. It reports to the business. And the results are concrete: their AI-powered next-best-action engine generates over S$150 million in incremental revenue annually, with hyper-personalized recommendations served to each customer based on their transaction patterns, life stage, and product holdings.

What makes DBS instructive isn’t the scale — it’s the loop. Their models don’t just predict. They act (through the digital banking app), measure (through real-time event capture), learn (through automated model retraining), and improve (through continuous A/B testing). They closed the loop between insight and action. That’s the octopus — distributed intelligence with coordinated intent.

Nubank in Brazil took a different path to the same destination. With 100+ million customers and no legacy core system, they built real-time credit decisioning that adjusts limits dynamically based on behavioral signals — not quarterly bureau pulls. A customer who pays their bill early three months in a row sees a limit increase surface before they ask. A customer whose spending patterns shift toward cash advances gets a preemptive financial health check, not a collections call. The intelligence isn’t bolted on. It’s native.

Now, neither DBS nor Nubank solved the complete problem. DBS has the models but not the coaching framework. Nubank has the behavioral data but not the executive command layer. What we’re building at Backbase is the architecture that unifies all of it — coach, orchestrator, command center, intelligence supply chain — into a single platform layer that any bank can deploy.

Here’s what it looks like.

The Architecture of Five Layers, One Closed Loop

My childhood was in middle east, where the bazaar is the original platform economy. In a grand bazaar, the merchant doesn’t wait for you to ask for saffron. He reads your gait. He notices you paused at the spice stall. He calculates, from your clothes and your hesitation, whether you’re buying for a wedding or for Tuesday dinner. He adjusts his pitch, his price, his product selection — in real time, with empathy, and with the explicit goal of making a sale while making you feel like you got exactly what you needed.

That’s what the Intelligence Layer does. Five architectural zones, each with a specific job, wired into a closed loop where insight becomes action becomes learning becomes better insight.

Zone 1. FullStoryAI — The Executive Command Center

This is not a dashboard. I need to be very precise about what this means, because the instinct of every bank CTO who hears “executive interface” is to imagine a dashboard with a chat window bolted on.

FullStoryAI is a contextually aware command center. It knows who you are (your role, your KPIs, your direct reports, your segments). It knows when you’re asking (Monday morning vs. quarter-end vs. the day before a board meeting). It knows what changed since you last logged in. And critically, it knows what you can do — not just what you can see.

When the Head of Retail opens FullStoryAI on a Monday morning, she doesn’t see a blank chat prompt. She sees: “142 savings closures over the weekend. 78% in your 25–34 segment. This coincides with Metro Bank launching a 5.15% HYS on Friday. 12,400 more customers match the at-risk profile. I have three response options ready.”

And in that same session — that same conversation — she can analyze the threat, compare response strategies, build a multi-channel campaign, approve it, and deploy it through the Engagement Banking Platform. Insight to action in one session. No Jira ticket. No six-month cycle. The competitive response is live before her 9 AM standup.

That’s Zone 1. It sits at the top of the architecture because it’s where human judgment meets machine intelligence. Everything below it exists to make this conversation informed and actionable.

Zone 2: The Products — Coach, CLO, and Conversational Banking

Here’s where the octopus metaphor earns its keep. Zone 2 has three products, each with its own neural cluster, each capable of independent action, but all coordinated by the same intent.

The Financial Coach is the customer-facing product. It delivers what I call “empathy at scale” — structured financial journeys (we call them “plays”) that guide customers toward financial health. (A simple capability demo.)

The Customer Lifetime Orchestrator (CLO) is the engine behind the Coach. Its Objective Plan Generator Agents and Asset Generator Agents drive the four lifecycle phases — Acquire, Activate, Expand, Retain — turning bank strategy into automated execution. (A simple capability demo.)

Conversational Banking provides the natural language interface for day-to-day banking operations, sitting on the same intelligence substrate as the Coach and CLO.

But the Coach is where the deepest technical and behavioral innovation lives. And it deserves a section of its own.

The Coach — A Technical Deep Dive Into Empathy at Scale

Most fintech companies use the word “coaching” the way fast food restaurants use the word “fresh.” It’s a label pasted on top of generic tips, spending summaries, and notifications that nobody reads. Real coaching — the kind that changes behavior — requires understanding three things simultaneously:

- what the customer should do,

- how to get them to actually do it, and

- when to intervene without creating fatigue or resentment.

That’s a neuroscience problem, an ML engineering problem, and a behavioral economics problem — all at once. The Coach architecture is designed to solve all three.

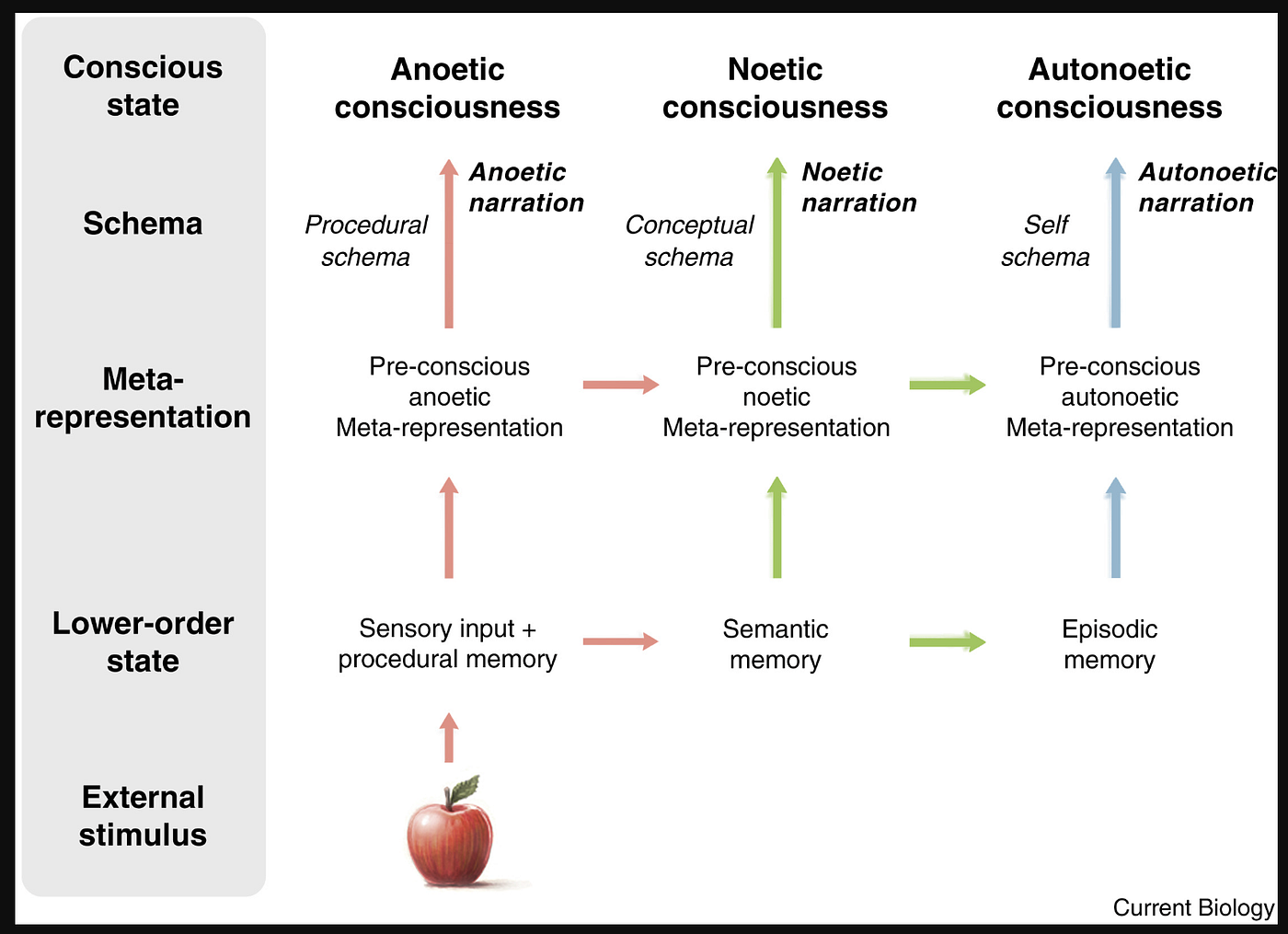

The Neuroscience of Financial Habit Formation

Before I explain the architecture, I need to explain why it’s shaped the way it is. The answer comes from neuroscience — specifically, from how the human brain forms, reinforces, and sustains habits.

In 2012, a team at MIT’s McGovern Institute published research on the basal ganglia — the brain structure responsible for habit formation. They found that habits follow a three-stage neurological loop: cue → routine → reward. A cue triggers the behavior. The routine is the behavior itself. The reward reinforces the neural pathway, making the behavior more likely to repeat.

This isn’t metaphorical. It’s structural. Habit formation literally rewires neural circuits through a process called long-term potentiation (LTP) — the strengthening of synaptic connections through repeated activation. Every time you perform a habit loop, the myelin sheath around the associated neural pathway thickens, making the signal faster and more automatic. This is why established habits feel effortless — the neural pathway has been physically optimized through repetition.

Now here’s the banking problem: financial behavior operates on exactly the wrong timescales for natural habit formation. You pay your mortgage once a month. You review your credit score quarterly. You think about retirement once a year, if that. The cue-routine-reward loop never fires frequently enough to build the myelin sheath. Financial behaviors remain decisions — conscious, effortful, easily disrupted — rather than habits — automatic, effortless, self-sustaining.

The Coach architecture is engineered to solve this. Each component maps to a specific stage of the neurological habit loop, running at frequencies that the natural financial cycle can’t provide.

The Three-Mesh Architecture

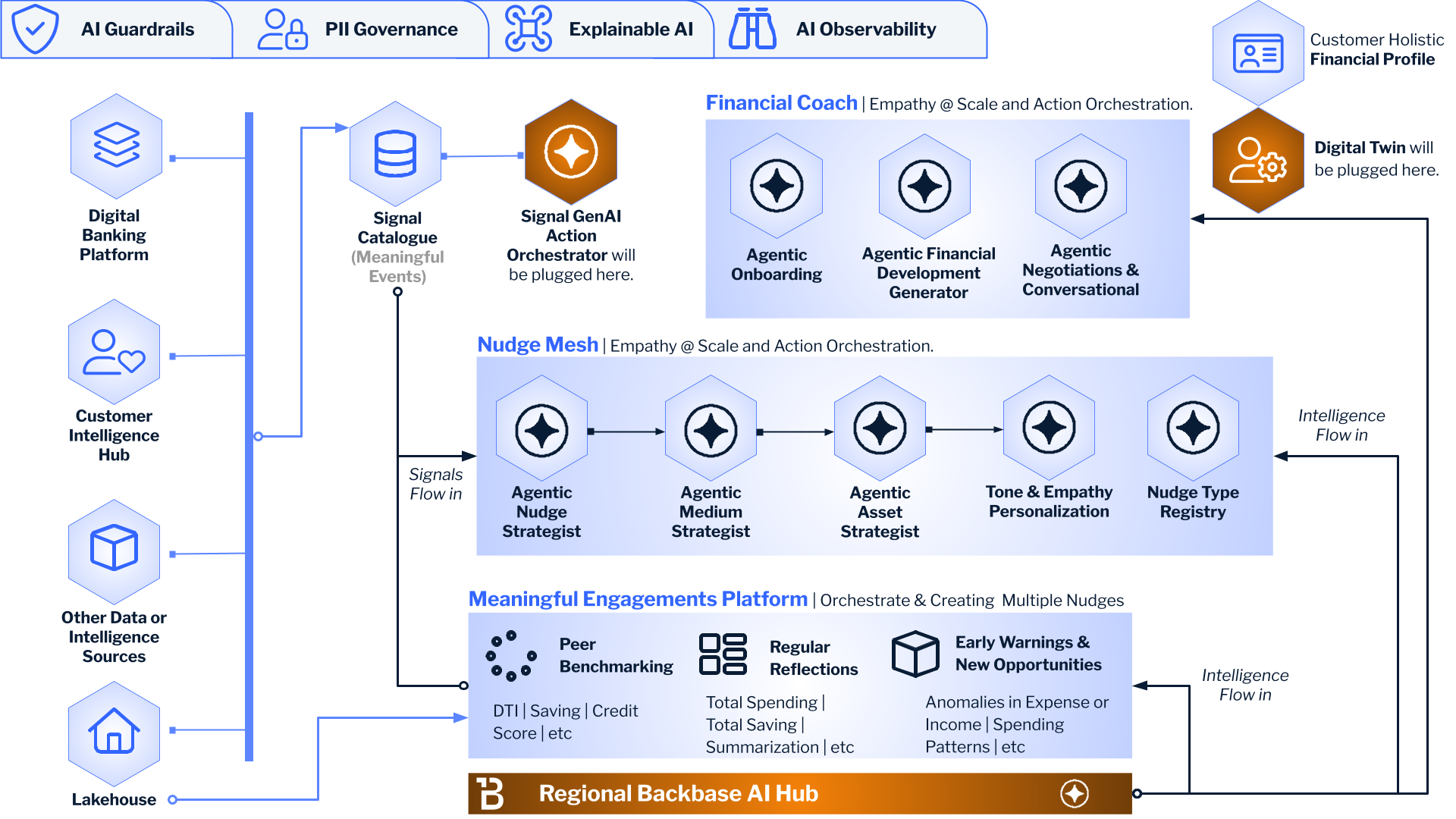

Looking at the Coach architecture diagram, you see three distinct mesh layers — the Coach Agent Mesh, the Nudge Mesh, and the Meaningful Engagements Platform — plus the data inputs on the left (Digital Banking Platform, Customer Intelligence Hub, external data sources, Lakehouse) and the intelligence components on the right (Digital Twin, Customer Holistic Financial Profile). The Signal Catalogue and Signal GenAI Action Orchestrator sit between the data inputs and the meshes, routing signals to the right agents.

This isn’t a random arrangement. Each mesh corresponds to a distinct cognitive function in the habit formation process.

Mesh 1: The Coach Agent Mesh — Establishing the Cue-Routine Map

The Coach Agent Mesh is the cognitive layer — it does the thinking. Three agentic systems work in sequence to build the customer’s financial roadmap.

01.Agentic Onboarding is the assessment engine. When a customer enters a play — say, Credit Score Forge — the onboarding agent pulls their credit bureau data, ingests their open banking transaction history, builds a behavioral credit proxy from their payment patterns, and generates an internal Credit Health Score.

From an ML perspective, this is a multi-modal feature engineering pipeline. The agent isn’t just aggregating data — it’s constructing a latent representation of the customer’s financial state. Transaction sequences are processed through a temporal convolutional network (TCN) that captures spending patterns across multiple time horizons (weekly, monthly, seasonal). Credit bureau data provides the static features. The behavioral credit proxy — our proprietary innovation — uses a variational autoencoder to learn a compressed representation of payment behavior that predicts creditworthiness even when traditional bureau data is thin or absent.

The output isn’t a number. It’s a state vector — a multi-dimensional representation of where the customer is financially. This vector becomes the starting node on their financial roadmap.

02.Agentic Financial Development Generator is the planning engine. It takes the state vector from onboarding and generates a personalized roadmap — a sequence of actions, milestones, and product adoptions that moves the customer from their current state toward their goal state.

This is where the architecture gets interesting from a reinforcement learning perspective. The roadmap isn’t a static checklist — it’s a policy generated by a planning agent that operates over a state-action space defined by the customer’s financial dimensions. The state space includes credit score, DTI ratio, savings buffer, product holdings, income stability, and 40+ other features. The action space includes financial behaviors (pay before statement close, reduce utilization below 30%, set up autopay), product adoptions (secured card, credit-builder loan, high-yield savings), and Coach interactions (schedule reflection, present simulation, deliver educational content).

The planning agent uses a variant of Monte Carlo Tree Search (MCTS) — the same family of algorithms that powered AlphaGo — to explore possible roadmap sequences and select the one that maximizes the probability of reaching the goal state within the customer’s timeline constraints. The key innovation: the reward function isn’t just score improvement — it incorporates engagement sustainability. A roadmap that delivers maximum score improvement but requires 15 actions per week will fail because the customer will disengage. The planner explicitly optimizes for the Goldilocks zone of challenge: enough to create progress, not enough to create fatigue.

In neuroscience terms, this maps to Vygotsky’s zone of proximal development — the sweet spot between what a learner can do independently and what they can do with guidance.

The Financial Development Generator keeps the customer perpetually in this zone: each milestone is achievable but stretching, creating the dopaminergic reward signal that reinforces the habit loop.

03.Agentic Negotiations & Conversational is the interaction engine. It handles the moments that require agent-level reasoning: presenting product offers with personalized terms, negotiating rate reductions with the bank’s pricing engine, initiating bureau dispute workflows, and managing complex multi-turn conversations where the customer’s emotional state matters.

This agent uses a fine-tuned large language model with a domain-specific reward model trained on banking conversation outcomes. The reward model doesn’t just optimize for task completion (“did the customer apply for the card?”) — it optimizes for relationship quality (“did the customer feel heard, respected, and informed?”). This is trained on conversation-level satisfaction signals derived from downstream behavioral outcomes: does the customer return to the Coach after this interaction? Do they complete their next milestone? Do they upgrade their tier?

The relationship-quality reward model is what separates an AI financial coach from an AI sales agent. Both can present a product offer. Only the Coach knows when presenting a product offer is the wrong thing to do — when the customer is stressed, grieving, or financially overwhelmed, and the right action is empathy, not optimization.

Mesh 2: The Nudge Mesh — Engineering the Cue Delivery System

If the Coach Agent Mesh is the brain, the Nudge Mesh is the nervous system. It has five components, each handling a specific dimension of message delivery.

01.Agentic Nudge Strategist decides what to nudge and when. This is the temporal orchestration layer — and it’s where the neuroscience of habit formation is most directly encoded.

The Nudge Strategist operates a reinforcement learning agent that learns each customer’s optimal nudge cadence. The state space includes: time since last nudge, engagement rate over rolling windows (3-day, 7-day, 30-day), current play phase, milestone proximity, and customer stress indicators (from transaction anomalies). The action space is: send nudge now (with type selection), delay nudge (with reschedule window), or suppress nudge entirely.

The reward function encodes the Yerkes-Dodson law from psychology — the inverted-U relationship between arousal and performance.

Too few nudges and the customer forgets, the habit loop doesn’t fire, the neural pathway doesn’t strengthen. Too many nudges and the customer experiences reactance — the psychological state where perceived pressure causes the opposite of the intended behavior. The RL agent learns to surf the peak of the inverted U for each individual customer.

From a practical standpoint: a Gen Z customer rebuilding credit might receive 3–4 nudges per week, mostly via push notification or other in-app capabilities, timed to late morning (their engagement peak). A pre-retiree on the Freedom Glide Path might receive one nudge per month via email, timed to the first business day after their paycheck (their action peak). The Nudge Strategist learns these patterns from behavioral data, not from demographic assumptions.

02.Agentic Medium Strategist decides where to deliver the nudge. This is a multi-armed bandit problem with contextual features. The arms are: push notification, in-app banner, email, SMS, and in-app message. The context includes: time of day, day of week, device type (mobile vs. desktop), historical channel engagement rates for this customer, and the urgency classification of the nudge (payment reminder = high urgency = push/SMS; educational content = low urgency = in-app feed).

We use a Thompson Sampling approach with Bayesian updating — each customer has a posterior distribution over channel preferences that updates with every interaction. This means the Medium Strategist’s channel selection improves with every nudge it sends. After 20–30 nudges, it has a highly accurate model of which channel this specific customer responds to for each type of message.

03.Agentic Asset Strategist assembles the content of the nudge. This is the generative layer. For a payment reminder, it constructs: the specific amount, the specific account, the specific date, and the specific impact (“paying $150 before Friday keeps your utilization below 30%, which protects your score improvement from last month”). For a milestone celebration, it constructs: the score change, the comparison to the starting point, the next milestone, and the products now unlocked.

The Asset Strategist uses a DCO (watch the sample demo, our key AI engineer behind this is Tram) and retrieval-augmented generation (RAG) pipeline grounded in the customer’s Digital Twin state. It doesn’t hallucinate financial advice — every claim about score impact, product eligibility, or savings amount is computed from the customer’s actual financial profile, verified against the bank’s product rules engine, and formatted for the Medium Strategist’s selected channel.

04.Tone & Empathy Personalization is the most nuanced component — and the one that most banking AI architectures completely ignore. It adjusts the emotional register of every message based on the customer’s inferred emotional state and the context of the interaction.

This is a classification problem solved by a sentiment-aware language model. The model takes three inputs: the customer’s recent behavioral signals (did they just miss a payment? did they just reach a milestone? have they been dormant for two weeks?), the demographic and psychographic profile from the CDP, and the content from the Asset Strategist. It outputs a tone vector across five dimensions: formality (casual ↔ professional), warmth (supportive ↔ neutral), urgency (gentle ↔ time-sensitive), celebration (muted ↔ enthusiastic), and complexity (simple ↔ detailed).

Why does this matter? Because of a neuroscience principle called state-dependent memory. Humans encode and retrieve information differently based on their emotional state. A customer who just missed a payment is in a shame-anxiety state. A celebratory, high-energy nudge in that moment doesn’t just feel wrong — it’s neurologically ineffective. The information won’t encode properly because the emotional state doesn’t match the message tone. The Tone & Empathy engine ensures tonal congruence: gentle and non-judgmental after setbacks, celebratory after milestones, educational during onboarding, calm and steady during market volatility.

The difference between a financial app that sends notifications and a Coach that builds habits lives in this layer. It’s the difference between a gym that sends you a “COME WORK OUT!” text after you’ve skipped three days (and which you’ll delete with resentment) and a trainer who texts “Hey, noticed you’ve had a tough week. When you’re ready, I’m here — even a 15-minute walk counts” (which makes you put on your shoes).

05.Nudge Type Registry is the configuration layer — the taxonomy of all nudge types available across all plays. Payment reminders, utilization alerts, milestone celebrations, bureau update notifications, product readiness alerts, peer comparisons, educational micro-lessons, dispute status updates. Each type has metadata: urgency classification, required Asset Strategist fields, permitted channels, frequency caps, and A/B test configurations. The Registry enables the Zero-Deployment Nudge Registry concept — when a new play is activated via Play Builder & Store, its nudge types are instantly available without engineering deployment.

Mesh 3: The Meaningful Engagements Platform — Engineering the Reward Loop

The third mesh is where the habit loop closes. If the Coach Agent Mesh establishes what to do and the Nudge Mesh delivers the cue, the Meaningful Engagements Platform delivers the reward.

In behavioral neuroscience, reward isn’t just about dopamine — it’s about prediction error. The brain’s reward system is most activated not by expected rewards, but by rewards that exceed expectations. Wolfram Schultz’s landmark research on dopaminergic neurons showed that once a reward becomes fully predicted, the dopamine response flattens to baseline. The reward still happens — but it stops reinforcing the behavior.

This is why loyalty programs lose effectiveness over time: the 2% cashback becomes expected, and the motivational signal dies.

The Meaningful Engagements Platform is designed to maintain positive prediction errors across three mechanisms:

01.Peer Benchmarking leverages social comparison theory — Leon Festinger’s 1954 framework that humans evaluate their own abilities and opinions by comparing with others. The Coach shows: “You’ve improved 45 points in 6 months. Others who started at your level averaged 38 points in the same period.”

The ML behind this is a cohort matching system. We construct comparison cohorts using a propensity score matching pipeline: customers are matched on starting score, income band, age bracket, geographic region, and play enrollment date. The resulting cohort comparison is statistically valid — not a cherry-picked “average” that makes everyone feel good. Some customers will be above their cohort. Some below. The honesty is critical: research on social comparison in health behavior (notably Cialdini’s work on energy conservation) shows that accurate social benchmarks change behavior while inflated ones do not.

From a prediction-error perspective, Peer Benchmarking creates variable reward: sometimes you’re ahead of your cohort (positive prediction error → dopamine → reinforcement), sometimes you’re behind (negative prediction error → motivation to close the gap). The variability itself is reinforcing — it’s the same mechanism that makes game leaderboards addictive. We’re using it to make financial health addictive.

02.Regular Reflections are scheduled metacognitive interventions — moments where the Coach asks the customer to step back and assess their progress. Monthly credit health reports. Quarterly deep reflections with plan recalibration. Annual comprehensive reviews.

The neuroscience here draws on Endel Tulving’s concept of autonoetic consciousness — the human ability to mentally travel through time and evaluate past actions in light of future goals.

Regular Reflections activate this capacity deliberately. The monthly report doesn’t just show numbers — it shows a trajectory: “In January you were here. Now you’re here. At this rate, you’ll be here by December.”

This is technically a time-series visualization problem solved by the Digital Twin’s simulation engine. The Twin projects the customer’s financial state forward under three scenarios: current trajectory (baseline), optimized trajectory (if they follow all Coach recommendations), and degraded trajectory (if they disengage). The three-line projection creates both motivation (the gap between current and optimized) and urgency (the gap between current and degraded). The Asset Strategist renders this as a visual in the reflection nudge, calibrated to the customer’s financial literacy level by Tone & Empathy.

03.Early Warnings & New Opportunities is the system that detects inflection points — moments where the customer’s financial trajectory is about to change, positively or negatively.

This is an anomaly detection pipeline running on the CDP event stream. We use an ensemble of three detectors: a statistical process control model (CUSUM) for detecting shifts in steady-state metrics (balance trends, spending patterns), a temporal autoencoder that flags unusual event sequences (missed payment following salary change following address change = potential life crisis), and a rule-based detector for known patterns from the Signal Catalogue (hard inquiry cluster = credit shopping = potential churn).

Early Warnings close the habit loop by providing immediate feedback — the most powerful reinforcer in behavioral science. B.F. Skinner demonstrated this in the 1930s, and every behavioral study since has confirmed it: the shorter the delay between action and consequence, the stronger the behavioral association. When a customer’s utilization spikes above their target on a Tuesday, the Early Warning fires by Wednesday morning — not in next month’s statement. The immediacy transforms “utilization management” from an abstract financial concept into a felt experience with real-time feedback.

New Opportunities operate on the positive side: when the customer’s score crosses a milestone, when a new product becomes eligible, when a peer benchmark improves. These create the variable-ratio reinforcement that behavioral psychology identifies as the most resistant to extinction. The customer never knows exactly when the next positive surprise will arrive — which keeps the habit loop cycling.

What a “Segment of One” Actually Looks Like

Let me make all of this concrete with a real customer journey.

Meet Priya. She’s 29, a graphic designer in Austin, opened a savings account and a basic credit card with her community bank six months ago. She’s got a 580 credit score — not terrible, but locked out of the financial products she actually needs. She’s been thinking about buying a condo but has no idea where to start.

Week 1: Agentic Onboarding kicks in. The moment Priya opens her savings account, the Coach detects: thin credit file, single product, 580 score, stable income via direct deposit (SalaryCredited events detected biweekly). The onboarding agent builds her state vector: thin-file, moderate income, low product density, high engagement potential (she logged in via mobile on day 1 — FirstLoginEvent). She's auto-enrolled into Credit Score Forge at Essential tier.

Week 2: First nudge. The Nudge Strategist fires her first cue — a push notification at 10:15 AM (her highest engagement probability, learned from her LoginFromMobile time patterns). The tone: warm, educational, zero pressure. "Your credit score journey starts today. One small step: we noticed your credit card utilization is at 68%. Bringing it below 30% could boost your score by 20-30 points. Here's how." The Medium Strategist chose push because Priya hasn't opened a bank email yet but opens push notifications within 3 minutes.

Month 2: Habit loop forming. Priya has received 7 nudges in 6 weeks — the Nudge Strategist’s RL agent determined her optimal cadence is slightly above once per week, biased toward Monday mornings. Her utilization dropped from 68% to 31%. Her score moved from 580 to 605. The Meaningful Engagements Platform fires her first Peer Benchmark: “You’ve improved 25 points in 6 weeks. Others who started where you did averaged 18 points.” Prediction error: positive. Dopamine: released. Habit loop: reinforced.

Month 4: Product coaching activates. The Financial Development Generator’s MCTS planner identifies her next optimal action: add a credit-builder loan to diversify her credit mix. The Product Coaching Layer — at Essential tier — tells her “a credit-builder loan could help.” But Priya upgraded to Premium after seeing the locked personalized roadmap. Now the Coach says: “The CreditStart Builder Loan at $1,000 for 12 months adds a new account type to your credit mix and costs $3.50/month in interest. Based on your trajectory, this moves your estimated qualification date for a mortgage pre-approval from March 2029 to November 2028 — five months sooner.”

That’s not a tip. That’s a financial development plan with a specific product, specific cost, and specific outcome tied to her stated goal.

Month 8: Score hits 640. Early Warning fires: “You’re 10 points from the 650 threshold that unlocks pre-approval for our HomePath mortgage program.” The Nudge Strategist increases cadence to twice weekly. Tone shifts from educational to motivational. Peer Benchmark shows she’s now in the top quartile of her cohort.

Month 12: Graduation. Score: 668. The Coach triggers the graduation ceremony: “One year ago you started at 580. Today you’re at 668. You’ve improved 88 points, you’ve added two credit products, and your DTI is 29%. You’re now eligible for mortgage pre-qualification.”

And here’s where the loop closes for the bank: the Coach routes Priya into the Mortgage Readiness play. FullStoryAI surfaces to the Head of Retail: “340 Credit Score Forge graduates this month qualify for Mortgage Readiness. Projected mortgage origination: $22M.”

Priya didn’t receive a single sales call. She was never “sold” a mortgage. She was coached into readiness — and the bank’s revenue grew as a direct consequence of her financial health improving. That’s the closed loop.

Signals That Feed the Meshes

The left side of the architecture shows four data sources that feed signals into the meshes:

01.The Digital Banking Platform generates behavioral events from the customer’s direct interactions — logins, page views, transactions, product applications, feature usage. These are high-frequency, low-latency signals.

02.The Customer Intelligence Hub (CIH) is the unified customer data layer — the CDP that aggregates and resolves customer identity across all touch points. The Signal Catalogue sits here: 60+ Meaningful Events across six categories (Acquisition & Onboarding, Product Holdings, Digital Engagement, Financial Transactions, Customer Service, Life Event Signals). Each event is a structured message with a schema, a confidence score, and a routing tag that the Signal GenAI Action Orchestrator uses to map it to the correct agent in the meshes.

03.Other Data or Intelligence Sources includes external data feeds: credit bureau APIs, open banking aggregation (account data from other institutions), market data (interest rate benchmarks, competitor product rates), and regulatory feeds.

04.The Lakehouse is the analytical data store — the historical depth that the real-time event stream doesn’t carry. It feeds the ML training pipelines for all three meshes and provides the long-lookback features (12-month spending trends, seasonal patterns, year-over-year comparisons) that the real-time stream can’t capture.

The right side of the architecture shows the Digital Twin and the Customer Holistic Financial Profile — the simulation and state-management layer that makes every Coach recommendation specific rather than generic.

The Digital Twin is a computational model of the customer’s financial life. It’s not a database record — it’s a simulator. It answers counterfactual questions: “If this customer pays $200 toward Card A instead of Card B, what happens to their credit score in 30 days?” “If this customer saves $500/month starting now, when do they have enough for a 20% down payment on a $350K home?” “If this customer’s employer match is 4% and they’re contributing 3%, how much retirement wealth are they leaving on the table over 20 years?”

The Twin runs different simulation engines depending on the play: a credit score factor model for Credit Score Forge, a debt amortization engine for Debt Freedom Engine, a Monte Carlo wealth projection for Freedom Glide Path, a cash-flow forecast for Liquidity Coach. Each engine is calibrated on real outcomes from the AI Hub’s proprietary ML models — the projections are grounded in what actually happened to similar customers, not in theoretical calculations.

The Intelligence Flow arrows on the architecture diagram show a bidirectional data path: signals flow into the meshes from the left (customer behavior → Signal Catalogue → agents), and intelligence flows back from the right (Digital Twin projections → Agent Mesh decisions → Nudge Mesh content). This bidirectional flow is the technical implementation of the habit loop: behavior generates signals, signals generate intelligence, intelligence generates nudges, nudges generate behavior.

Zone 3: The Intelligence Substrate

Six components, three current and three roadmap:

The Signal Catalogue, Signal Detection, and Signal Action Plan process behavioral events in real-time, applying pattern recognition and routing signals to the correct agents.

The Signal GenAI Action Orchestrator (roadmap) will auto-map novel signal combinations to agents on the fly — the shift from configured rules to generative reasoning.

The Ontology Sniff Tool (roadmap) will auto-generate event mappings from raw data sources, eliminating the data engineering bottleneck.

The Digital Twin provides the simulation engine described above.

Zone 4: The Backbase AI Hub

At the bottom of the Coach architecture sits the Regional Backbase AI Hub — the “Banking Hugging Face” that powers all the models and agents in the three meshes.

Three pillars today, one on the roadmap:

01.Proprietary MLs — thousands of models purpose-built for banking: churn prediction, credit scoring, transaction categorization, anomaly detection, next-best-action, spending pattern classification. These aren’t general-purpose models fine-tuned for banking. They’re trained on banking data, optimized for banking latency requirements, and validated against banking regulatory constraints.

02.Proprietary SLMs & Agents — domain-specific small language models that understand banking context natively. When a customer says “I’m worried about making rent this month,” a general-purpose LLM hears a statement. Our banking SLM hears a signal: potential missed payment risk + financial distress + possible churn + Resilience Shield activation opportunity.

03.Localized Trainings — regional models for US, EU, SEA, LATAM. Credit scoring works differently in every country. Tax obligations differ. Regulatory frameworks differ. A Coach play that works in Manhattan doesn’t work in Manila without localized intelligence.

04.On the roadmap: The GenAI Decision Suite — a web of agents that automatically evaluates which model on the AI Hub can best serve each specific agent in the meshes. When a better churn model is trained, the Suite evaluates it, A/B tests it, and deploys it — continuously boosting intelligence without human intervention.

Zone 5: The Integration Layer

External app integration (QuickBooks, Xero, Salesforce), workflow automation, and system connections: Core Banking, CRM, Cards, Payments, KYC, Fraud, Documents, Case Management, Lending, Treasury. Architecturally straightforward. Strategically critical — every layer above is only as good as the data flowing up from here.

The Closed Loop Nobody Else Has

The Intelligence Layer is a closed loop. The Coach nudges a customer. The customer acts. The CDP captures the action. Signal Detection processes it. The Digital Twin updates. The Coach adjusts. The CLO recalculates lifetime value. FullStoryAI surfaces the pattern to the Head of Retail. The Head of Retail activates a new play. The Nudge Registry deploys it. The Coach nudges a new cohort. Loop continues.

And the commercial engine: Play Builder & Store. When 3,200 customers graduate past a threshold and the bank doesn’t have the downstream play, FullStoryAI tells the CEO: “3,200 ready for mortgage coaching. Projected origination: $18–24M. Activate 90-day trial?” One click. No SOW. No engineering. Play deploys in 24 hours.

The platform sells itself.

What Nobody Wants to Talk About

This is the section most AI articles skip. The architecture above is a blueprint. Blueprints don’t build buildings — construction crews do. And in banking, the construction crew faces four types of friction that no architecture diagram can solve.

The Black Box Problem — Why Your Regulator Won’t Sleep Well

Let me put this bluntly: if you can’t explain why your AI denied a credit product, upgraded a customer, or routed someone into a specific Coach play, your regulator will shut you down. And they should.

Banking is not a domain where “the model says so” is an acceptable answer. The CFPB, OCC, FDIC, and their counterparts in every regulated market require adverse action explanations, fair lending documentation, and evidence that your AI systems don’t discriminate against protected classes — whether intentionally or through proxy variables that correlate with race, gender, age, or geography.

The Intelligence Layer is designed with explainability as a structural requirement, not a post-hoc addition. Here’s how:

The Product Coaching Layer’s mandatory net-benefit check runs a cost-benefit calculation before every product recommendation. If the cost of a recommended product (fees, interest, opportunity cost) exceeds the projected benefit, the recommendation is suppressed. This isn’t just good ethics — it’s a regulatory firewall. Every suppressed recommendation is logged with the calculation that triggered it. When an examiner asks “why didn’t you recommend Product X to Customer Y?”, the answer is documented: “because the net-benefit check determined that the $49 annual fee exceeds the projected $31 annual reward value for this customer’s spending pattern.”

Fair lending analysis runs continuously on Coach outputs. FullStoryAI’s Risk & Compliance Sentinel play monitors every product recommendation across demographic segments. When it detects disparate impact — say, Hispanic customers receiving credit-builder loan recommendations at 11% lower rates than White customers with similar profiles — it doesn’t just flag the issue. It diagnoses the root cause. In one of our prototype analyses, the disparity wasn’t algorithmic bias — it was a product availability gap. The credit-builder loan wasn’t offered at three branches serving predominantly Hispanic communities. The fix was operational (expand product availability), not algorithmic (retrain the model). That distinction matters enormously to examiners.

Every Coach decision is decomposable. The MCTS planner that generates financial roadmaps produces not just the optimal path but the decision tree it explored. When a customer asks “why did you recommend a secured card instead of a regular card?”, the Coach can show the specific factor weights: “your utilization is at 68% (factor weight: 0.35), your file age is 6 months (factor weight: 0.15), and secured cards have a 94% approval rate at your profile vs. 12% for unsecured (factor weight: 0.50).” The Digital Twin’s simulations are similarly transparent — every “if you do X, your score changes by Y” claim is traceable to the underlying model coefficients.

The AI Guardrails, PII Governance, Explainable AI, and AI Observability strip at the top of the architecture diagram isn’t decoration. It’s infrastructure. AI Guardrails enforce content safety and response boundaries. PII Governance ensures that customer data flows through the meshes without leaking personal identifiers into model training. Explainable AI generates human-readable decision rationales for every agent action. AI Observability monitors model drift, latency, error rates, and bias metrics in production.

For the CRO reading this: the Intelligence Layer doesn’t make your job harder. It makes it possible. Today, you’re trying to audit decisions made by humans who can’t explain their own reasoning (“I just had a feeling about that customer”). Tomorrow, you’re auditing decisions made by agents that produce complete audit trails, document every factor weight, and run fair lending analysis continuously rather than annually.

The Build vs. Buy Reality

Every Chief AI Officer and CTO reading this is asking the same question: “Do we build this, buy it, or partner for it?” Let me save you 18 months of analysis paralysis.

01.You cannot build the Intelligence Layer from scratch. Not because you lack talent — you probably have excellent data scientists. But because the Intelligence Layer isn’t a model or an app. It’s a platform layer that requires simultaneous integration across your core banking system, your digital channels, your CDP, your lending engine, your campaign management, and your compliance infrastructure. DBS Bank spent a decade and hundreds of millions getting to their current state — and they started as a well-funded government-backed institution with a mandate to digitize. Your community bank or mid-tier regional doesn’t have that runway.

02.You cannot buy it from a big cloud provider. AWS, Google Cloud, and Azure will sell you ML infrastructure — SageMaker, Vertex AI, Azure ML. These are excellent model training and serving platforms. They are not banking platforms. They don’t know what a Coach play is, what a Nudge Mesh does, or how to route a MaritalStatusUpdated signal into a Family Financial Orbit enrollment. They sell picks and shovels. You need a house.

03.You cannot assemble it from fintech point solutions. Plaid gives you account aggregation. MX gives you transaction categorization. Personetics gives you insights. Salesforce gives you campaign management. Each is good at one thing. None of them connect. And the integration lift of wiring seven fintech APIs into a coherent intelligence loop will consume your engineering team for two years while delivering none of the closed-loop value.

The answer is a platform partner that provides the architecture and the intelligence supply chain — where you bring the data and the domain specificity. This is what the Backbase AI Hub model is designed for. The Hub provides the proprietary MLs, the SLMs, the agent frameworks, and the localized trainings. Your bank provides the segmentation & CVPs, customer data, the product catalogue, the regulatory context, and the market knowledge. The Coach plays are configurable, not custom-built. The Nudge Mesh learns from your customers’ behaviors, not from generic benchmarks. The Zero-Deployment Nudge Registry means new plays activate without engineering sprints.

The analogy I use: you don’t build your own electrical grid to power your house. You plug into the grid. But you choose your own appliances, set your own thermostat, and decide which rooms to light. The Backbase AI Hub is the grid. The Coach plays are the appliances. Your data is the electricity.

The Cultural Vault

I spent years as CTO at Techcombank and Chief Digital Banking Officer at HDBank — two Vietnamese banks at very different stages of digital maturity. And I can tell you from direct experience: technology is the easy part of transformation. People are the hard part.

You have two populations inside your bank that don’t speak the same language:

Traditional bankers rely on relationships, intuition, and established rules. They’ve been successful for 20 years by knowing their customers, reading body language, and making judgment calls. When you tell them “an AI agent will now handle product recommendations,” they hear “you’re replacing me with a robot.” Their resistance isn’t irrational — it’s existential.

Data scientists rely on probabilistic models, feature importance scores, and A/B test results. They’ve been frustrated for three years because their models never reach production and the business doesn’t understand p-values. When you tell them “build a model that the branch manager will trust,” they hear “dumb it down.” Their frustration isn’t irrational either — it’s the gap between capability and deployment.

The Intelligence Layer only works if both populations trust its outputs. Here’s how to bridge the gap:

For the traditional bankers: the Coach doesn’t replace the RM. It arms the RM. At the Signature tier, the Coach’s output flows to the relationship manager, not instead of them. When a Coach play detects that a customer is mortgage-ready, the RM gets a briefing: “This customer has been in Credit Score Forge for 12 months. Score improved from 580 to 668. DTI is 29%. Savings velocity is $850/month. They searched for ‘first-time buyer programs’ last week. Here’s the talking points for your call.” The RM still makes the call. The RM still builds the relationship. But they walk in with intelligence they never had before.

The frame shift is: AI as augmentation, not automation. The best RMs will be the ones who learn to use Coach intelligence as a competitive advantage — who show up to customer meetings with insights that make them look brilliant. The ones who resist will be outperformed by the ones who adopt. That’s cultural evolution, not cultural replacement.

For the data scientists: the Intelligence Layer gives your models a production path. Your churn model doesn’t live in a Jupyter notebook anymore — it lives inside the Nudge Mesh, triggering retention plays, presenting competitive offers, and reporting its impact through FullStoryAI. The model’s success isn’t measured by AUC-ROC. It’s measured by retained revenue. That’s the metric that gets you a seat at the leadership table.

For the CEO: the cultural work is change management, not technology management. Budget 30% of your Intelligence Layer investment for people — training programs, incentive realignment, and organizational design changes. The Head of Retail’s team needs to learn how to commission Coach plays. The RM team needs to learn how to consume Coach briefings. The data team needs to learn how to operate the intelligence supply chain, not just build models. None of this happens with a technology deployment. It happens with leadership, role modeling, and patient iteration.

A bank I admire in this regard is Capital One. Their transformation wasn’t primarily about technology — it was about hiring. They brought in thousands of engineers and data scientists and put them inside the business units, not in a separate tech division. The cultural integration happened because the populations were forced to collaborate daily, not because someone issued a memo about “data-driven culture.”

The 90-Day Thin Slice

CEOs and CFOs want timelines. Ripping out a core system takes 5–10 years and has a failure rate that should make any board nervous. But the Intelligence Layer doesn’t require a core replacement. It sits above the core — which is both its architectural advantage and its fastest path to ROI.

Here’s the realistic roadmap:

Weeks 1–4: The Thin Slice. Pick one product line. Credit cards are the best candidate for most banks — high transaction volume, clear activation metrics (card activated, added to mobile wallet, first purchase within 7 days), and immediate revenue impact. Deploy the Coach with a single play: a credit card activation and engagement journey. Connect the CDP events you already have (CardIssued, CardActivated, TransactionAdded). Configure the Nudge Mesh for three channels (push, in-app, email). Run against a control group.

Weeks 4–12: Measure and Prove. You’re comparing Coach-nudged customers against the control group on: activation rate, time-to-first-purchase, mobile wallet adoption, monthly transaction volume, and 90-day attrition. Based on aggregate data from similar deployments, expect: 40–55% activation improvement for non-activators, 2.3x higher mobile wallet adoption, and 25% lower 90-day attrition.

Month 4–6: Expand the Slice. With proven ROI on one play, expand to Credit Score Forge (credit building) and Simple Financial Coaching (savings behavior). These two plays generate the data that makes downstream plays valuable — they’re the feeder plays that build the customer intelligence your Coach needs.

Month 6–12: Activate the Loop. Deploy FullStoryAI for the Head of Retail and Head of Segment. Connect the Mortgage Readiness play as the first downstream graduation target. Now you have the complete closed loop: feeder play → graduation signal → downstream play → product origination → revenue attribution.

Month 12+: Scale. At this point, you’re not pitching the board on an AI investment. You’re showing them a revenue engine with measured ROI: “Credit Score Forge graduated 340 customers to mortgage readiness this quarter. Coach-attributed mortgage origination: $4.2M. Cost of Coach platform: $X. ROI: Y%.” The board doesn’t need to take a leap of faith. They’re looking at a P&L.

The critical principle: never deploy the Intelligence Layer as a technology project. Deploy it as a commercial experiment with a control group, a 90-day measurement window, and a kill criterion. If it doesn’t prove ROI on the thin slice, you’ve lost 90 days and a limited investment. If it does — and the data consistently shows it does — you’ve earned the right to scale.

What This Means For You

Every bank executive reading this is in one of five roles. Each sees a different dimension of the Intelligence Layer — and each has a different reason to move now.

For the Chief AI Officer: The End of the Model Zoo

You’ve spent the last three years building models. You have a churn model, a next-best-action model, a credit scoring model, a fraud detection model. Some work. Some don’t. None of them talk to each other. Your data scientists are brilliant and frustrated — they build models that never reach production because the integration lift is six months and the business case dies in the gap.

The Intelligence Layer eliminates this gap. Your models plug into the AI Hub. The Hub’s agents serve them to the Coach, the CLO, and FullStoryAI through a standardized intelligence supply chain.

But here’s the harder truth: the model is not the product. You’ve been treating AI as a technology capability. It’s not. It’s a revenue capability.

The Intelligence Layer forces this reframe because every model connects to a customer action, and every customer action connects to a product outcome. Your churn model doesn’t live in a notebook anymore — it lives inside the Nudge Mesh, triggering retention plays, presenting competitive offers, and reporting its impact to the Head of Retail through FullStoryAI. The model’s success isn’t measured by AUC-ROC. It’s measured by retained revenue.

Stop building models that prove AI works. Start building models that prove AI earns. The Intelligence Layer gives you the architecture to connect every model to a revenue outcome. If you don’t make this shift, the next budget conversation will be your last as a C-suite function.

For the Chief Data Officer: The Signal Is the Strategy

You’ve been building a data lake, and you’re drowning in it. Your team spends 70% of its time on data engineering — building pipelines, fixing schemas, reconciling data from seven different source systems — and 30% on the analysis that actually matters.

The Intelligence Layer inverts this ratio.

The Signal Catalogue isn’t just an event taxonomy — it’s a strategic framework. Every Meaningful Event maps to a business intent. SalaryChanged isn't a data point — it's the entry signal for four different Coach plays. Your data has always had this meaning. The Intelligence Layer makes it explicit.

The Ontology Sniff Tool is your liberation from the pipeline treadmill. And the CDP becomes a Knowledge Graph for Agents — live substrate that every Coach agent, every CLO plan generator, and every FullStoryAI conversation queries in real-time.

Reposition the data function from “we manage data” to “we power the intelligence supply chain.” The CDO who owns the Signal Catalogue, the CDP knowledge graph, and the Ontology Sniff Tool isn’t running a support function — they’re running the input layer of the bank’s revenue engine.

For the CEO: The Platform That Sells Itself

You’re tired of technology investments that require faith. Every AI pitch you’ve heard follows the same pattern: big promise, big budget, vague ROI, two-year timeline, and a “we’ll show value in phase 2” caveat.

The Intelligence Layer breaks this pattern because the ROI is structural, not speculative.

The Coach enrolls a customer into Credit Score Forge. Over 12 months, the customer’s score improves from 520 to 680. The Coach’s product coaching layer presents a specific credit card matching their spending pattern, at the specific moment their score qualifies. Conversion rate: 3–4x higher than cold marketing. Default rate: 35% lower because the customer was coached into readiness, not sold into risk.

Now multiply by 11 retail plays and 10 SME plays. Each play is a revenue pathway that compounds.

And then there’s Play Builder & Store — where your own customer data creates the sales trigger. “680 customers have graduated Credit Score Forge with homeownership intent. Mortgage Readiness play available. Projected origination: $18–24M. Activate?” You click yes. Play deploys in 24 hours. No SOW. No implementation project.

Stop evaluating AI as a technology decision. The question isn’t “should we invest in AI?” It’s “do we want a banking platform where coaching customers toward financial health is the same motion as growing our revenue?”

For the Head of Retail: Your Monday Morning Just Changed

You arrive at 8:15 AM. You open FullStoryAI. Before you ask a single question, it tells you:

“142 savings closures over the weekend. 12,400 more at risk. Three response options ready. My recommendation: targeted retention combined with Coach enrollment. Want me to build the campaign?”

You tap yes. Campaign deploys before your 9 AM standup. You ask for a 35-second talking point about the competitive response. You walk into the meeting prepared.

But it goes deeper than speed. The Coach is doing something for your customers that you’ve never been able to do at scale: build genuine financial health. And the commercial insight is that financial health and revenue growth are the same thing. A customer who builds their credit score becomes eligible for your mortgage products. A customer who eliminates debt frees cashflow that becomes your deposits, your AUM, your insurance premiums. The Coach creates the customer you wish you had.

Push for FullStoryAI as the replacement for the dashboard-and-meeting cycle that costs you 2–3 weeks of reaction time on every competitive move. The bank that responds in hours will take market share from the bank that responds in weeks.

The Only Architecture Where Everyone Wins

I want to end with something I’ve been thinking about since my years building digital banking in Vietnam. In most technology architectures, there’s an inherent tension between what’s good for the customer and what’s good for the business. The product team wants engagement. The finance team wants revenue. The compliance team wants less risk. The risk team wants explainability. The RM wants to keep their job. These goals pull in different directions, and the architecture becomes a series of compromises.

The Intelligence Layer is the first architecture I’ve seen where these goals are structurally aligned:

The customer gets wealthier — better credit, less debt, a clearer path to homeownership, a more resilient financial life.

The bank gets richer — higher product density, better conversion rates, lower defaults, more AUM, deeper relationships.

The regulator gets transparency — explainable decisions, documented audit trails, continuous fair lending analysis, and a system that suppresses recommendations when the customer doesn’t benefit.

The RM gets superpowers — walking into customer meetings with intelligence they never had, armed with specific insights and pre-built talking points.

The platform gets smarter — every customer action teaches the models, every executive decision feeds back into the intelligence substrate, every rotation of the loop improves the next rotation.

All five happen in the same motion.

That’s not an incremental improvement on banking technology. That’s a new category. And the banks that move first — starting with a thin slice, proving ROI in 90 days, and scaling from evidence — will define it.

The others will be reading about it in next year’s analyst reports, wondering why their dashboard didn’t warn them.