There’s a man in the bazaar who has been buying saffron from the same merchant for thirty years. He doesn’t browse. He doesn’t compare. He walks in, the merchant has already weighed his usual order, adjusted for the season, set aside the grade he prefers. The merchant knows his holidays, his family size, whether he’s cooking for guests or for Tuesday dinner. The transaction takes ninety seconds. The relationship took three decades to build.

Now imagine a version of that merchant who works for you — not for the bank. An agent who knows your finances the way that merchant knows saffron: what you need, when you need it, and what you’d never accept. An agent who doesn’t wait for you to open the app. An agent who acts on your behalf, within rules you define, 24 hours a day.

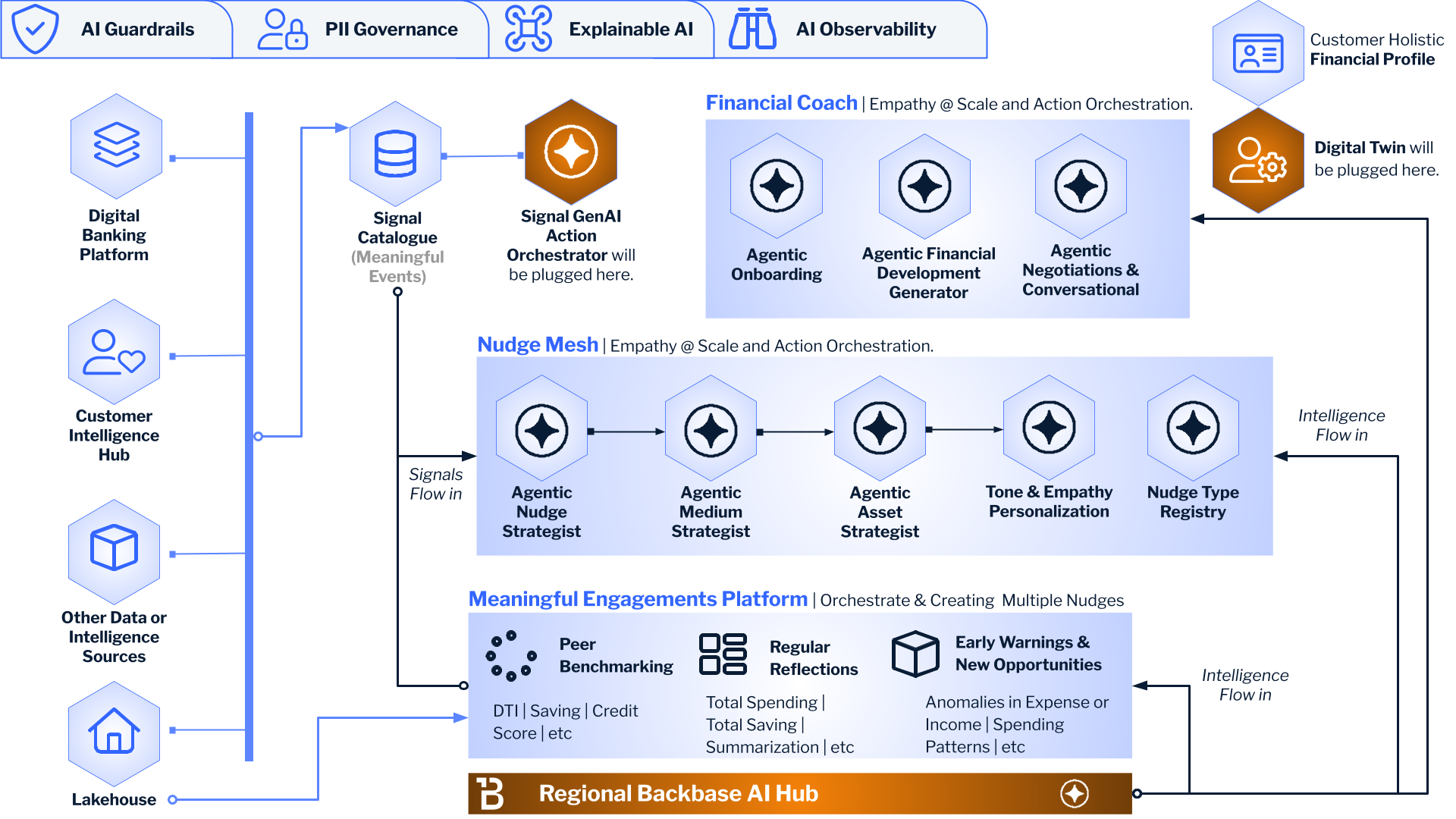

That’s not a banking app. That’s a Digital Twin.

And it’s the end of mobile banking as we know it.

The Problem With Every Banking App Ever Built

Every banking app in existence follows the same model: the customer opens the app, performs an action, closes the app. Check balance. Transfer money. Pay a bill. The app is a tool. The customer is the operator. Every action requires the customer to initiate.

This model made sense when the alternative was a branch visit. It made sense when “mobile banking” was a competitive differentiator. It no longer makes sense.

Here’s why: the average banking customer opens their app 2–3 times per week. They spend approximately 4 minutes per session. That’s 8–12 minutes per week of active engagement with their financial life. During those 8–12 minutes, they’re checking balances and making transfers — the financial equivalent of checking the rearview mirror. They’re looking backward at what already happened.

Meanwhile, their savings account rate dropped 30 basis points last month and they didn’t notice. A subscription they forgot about has been charging $14.99 monthly for six months. Their credit card’s annual fee exceeds their rewards value by $33. A CD matured and the funds are sitting in a 0.01% holding account. A competitor is offering a rate 85 basis points higher than their current savings product.

The customer doesn’t know any of this. Not because they’re financially illiterate — because the information requires active effort to discover, and the app only works when the customer operates it.

The Digital Twin inverts this model entirely.

What a Digital Twin Actually Is

The Digital Twin is not a dashboard with better charts. It’s not a “financial insights” feature. It’s not a chatbot that summarizes your spending.

The Digital Twin is your autonomous financial agent — an AI clone that operates under a delegated authority framework. Think of it as a digital Power of Attorney: you grant your Twin authority to act on your behalf, within rules you define, subject to constraints you set, with the ability to revoke at any time.

The customer doesn’t need to open the app anymore. The Twin opens the app for them — monitoring, optimizing, executing, and negotiating 24/7. The customer is only pulled in when the Twin needs a decision that exceeds its delegated authority, or when the customer wants to adjust the rules.

This is the shift from “the bank has an app that the customer uses” to “the customer has an agent that uses the bank.”

And it demands an entirely new set of KPIs. The metrics that defined success in digital banking for the past decade — monthly active users, login frequency, page views — measure how often the customer operates the tool. In a Digital Twin world, the customer doesn’t operate the tool. The Twin does. Measuring logins is like measuring how often a CEO visits the factory floor: it tells you nothing about whether the factory is producing.

Here’s how the measurement framework shifts:

Why this matters for your board deck

The old scorecard answered: “Are customers using our app?”

The new scorecard answers: “Is our platform making customers wealthier and the bank richer — simultaneously?”

When you present Digital Twin metrics to a board, you’re not showing engagement charts that require faith to connect to revenue. You’re showing: “$847 average annual value per Twin-active customer. 4.2x product acceptance rate via negotiation. 0.3% churn rate for Twin-active vs. 4.1% for non-active. $12.4M in Twin-attributed revenue this quarter.”

That’s not a digital banking report. That’s a P&L.

The Power of Attorney Framework

The governance model borrows from a concept every adult understands: the Power of Attorney.

In traditional POA, a human grants another human authority to act on their behalf, within defined scope, subject to defined constraints, with the ability to revoke at any time. Your estate attorney can sign documents for you. Your healthcare proxy can make medical decisions. Both operate within boundaries you defined.

The Digital Twin applies the same framework to AI:

Grantor: You, the customer.

Agent: Your Digital Twin.

Scope: Which domains the Twin can act in — savings, bills, subscriptions, investments, credit, insurance. You choose.

Constraints: The rules and limits you define. “Never let my checking balance drop below $3,000.” “Never lock money for more than 18 months.” “Never accept an interest rate below 3%.” “Always ask me before committing to anything over $500.”

Autonomy levels: You choose how much freedom the Twin gets, domain by domain:

Monitor only — the Twin watches and alerts but never acts. Good for customers who want visibility without automation.

Recommend and wait — the Twin proposes an action and waits for your approval. Good for high-value decisions like product switching.

Recommend and act — the Twin acts within your rules and notifies you afterward. Good for recurring optimizations like CD laddering.

Full auto — the Twin operates autonomously and reports in a weekly digest. Good for routine operations like bill payment.

Revocation: You can narrow, expand, pause, or revoke the POA at any time, instantly. One tap. No waiting period.

This isn’t a theoretical framework. It maps directly to how modern AI governance systems work — the customer’s constraints become policies, the Twin’s actions require authorization tokens, and every action is logged, explainable, and auditable.

The Five Capabilities

1. The Financial Simulation Engine — “What Could Be True Tomorrow”

Before the Twin acts, it thinks. And “thinks” means: it runs a computational simulation of every possible action and selects the one that best serves your goals within your constraints.

This isn’t a rule-based optimizer that checks “is 4.2% greater than 3.8%?” It’s a multi-model simulation engine:

A credit score factor model that decomposes your score into contributing factors and projects how each possible action would change it. “If you pay $200 extra toward Card A instead of Card B, your score improves 15 points more — because Card A’s utilization impact is larger at your current balance.”

A cash flow forecast that predicts your income and expenses over the next 3–12 months, using your transaction history. It knows your salary timing, your seasonal spending patterns, your recurring bills. When the Twin considers locking $5,000 in a CD, it first verifies that you won’t need that cash based on projected outflows.

A debt amortization engine that models every debt instrument you hold and runs payoff optimization scenarios. Which debt should you prioritize? The one that minimizes total interest? The one that maximizes credit score improvement? The one that frees cash flow fastest? The answer depends on your goals, and the engine runs all three scenarios.

A wealth projection engine that runs Monte Carlo simulations on your investments, retirement accounts, and savings goals. Not point estimates — probability distributions. “There’s an 85% chance you’ll have between $1.2M and $1.8M at age 65 under current contributions.”

A product eligibility forecaster that projects when you’ll qualify for products you don’t currently have access to. “At your current trajectory, you qualify for the Platinum card in 4 months and mortgage pre-qualification in 11 months.”

The Simulation Engine is the foundation. Every autonomous action the Twin takes is first simulated. The Twin never acts on heuristics. It acts on computed outcomes.

2. The Autonomous Optimizer — “Do This For Me”

This is where the Twin becomes genuinely autonomous. You delegate specific optimization mandates, and the Twin executes continuously.

Savings and CD optimization: “Maximize my interest income. Never let checking drop below $3,000. Never lock money for more than 18 months. Never accept below 3%.”

The Twin continuously monitors available CD rates, your cash flow forecast, and maturity laddering opportunities. When it identifies an optimization move, it executes — no customer interaction needed. You see a notification: “Moved $2,500 into a 9-month CD at 4.35%. Your projected annual interest income increased by $108.”

Bill payment and subscription management: “Pay all recurring bills automatically. Flag anything over $100/provider/month. If you find duplicate subscriptions, research which is better and let me decide.”

The Twin monitors recurring charges, detects duplicates (two streaming services, two cloud storage plans), tracks price increases, and flags services you haven’t used in 90+ days. For duplicates, it researches both services and presents a comparison: “You’re paying for Spotify Premium ($14.99/mo) and Apple Music ($10.99/mo). Based on your usage patterns, 85% of streaming transactions are Spotify. Recommend canceling Apple Music. Annual savings: $131.88. Approve?”

Credit card optimization: “If my annual fee exceeds my rewards value, negotiate a fee waiver or suggest switching.”

The Twin tracks your spending patterns by category, calculates your actual rewards earnings against fees, and alerts you when the math stops working. Better: it can request a fee waiver based on your relationship history. “Your card costs $95/year but you’re earning $62 in rewards. I’ve requested a fee waiver based on your 3-year relationship and $45K in deposits. Waiver approved — saving you $95/year.”

3. The Negotiation Agent — “Negotiate For Me”

This is the capability that doesn’t exist anywhere else in banking — and the one that creates the deepest competitive moat.

The Digital Twin negotiates with the bank’s own AI systems on your behalf.

Here’s how it works: the bank’s customer lifetime orchestrator generates a product offer for you — say, a Platinum credit card with a $95 annual fee and 2% cashback. Normally, this offer appears in your app as a banner or notification. You see it, you accept or ignore it.

With the Digital Twin active, the offer is intercepted by your Negotiation Agent first. The Twin evaluates: your assets under management are $85K. Your tenure is 4 years. You hold 3 products. Your POA rule says: “Accept credit card offers only if the fee is waived or rewards exceed the fee by 2x.”

The Twin responds to the bank’s system: “My client has $85K in assets and a 4-year relationship. The annual fee makes this offer net-negative at their spending level. Waive the fee and my client accepts. Otherwise, we pass.”

The bank’s pricing engine evaluates: the lifetime value of retaining this customer with a Platinum card (higher interchange, deeper relationship, lower churn probability) versus the $95 fee waiver. The math works. Fee waived. Twin accepts on your behalf.

You get a notification: “Negotiated a fee waiver on the Platinum card based on your account history. Card activated. Annual savings: $95.”

This is bilateral AI negotiation — your agent and the bank’s agent, each optimizing for their principal, reaching mutually optimal terms instantly and rationally. You get better terms. The bank gets higher acceptance rates. Both sides win because the negotiation happens without the friction, delay, and emotional baggage of human-to-human negotiation.

Think about what this means at scale. Today, banks send millions of product offers with single-digit acceptance rates. Most offers are ignored because the terms don’t quite fit. With Digital Twin negotiation, every offer becomes a conversation — the Twin counter-offers, the bank’s system evaluates, and the terms adjust until they work for both sides or the Twin walks away. Acceptance rates multiply. Customer satisfaction increases. Revenue per offer increases. The waste in the current spray-and-pray model disappears.

4. The Guardian — “Protect Me”

The Digital Twin doesn’t just optimize. It watches your back.

Fraud and anomaly detection: Unusual transaction at an electronics store in a city you haven’t visited? The Twin freezes the card in seconds — not hours — alerts you, and initiates a dispute if you confirm it’s unauthorized. Speed matters. The Twin acts while you’re sleeping.

Lifestyle creep detection: Your dining spending increased 40% over three months without a corresponding income increase. The Twin flags it: “At this rate, your savings contribution drops below your $500/month target by June. Want me to set a dining budget alert?” This isn’t judgment. It’s math. The Twin knows your goals and sees the trajectory diverging.

Rate and fee erosion: Your savings account rate dropped from 4.1% to 3.8% last month. Most customers never notice. The Twin notices immediately and presents options: “A 12-month CD at 4.3% is available. Based on your cash flow forecast, you can lock $8,000 without hitting your liquidity floor. Want me to move it?”

Subscription surveillance: A free trial converted to a $19.99/month charge. A service you haven’t used in 4 months is still billing. A provider increased their price by $3/month. The Twin catches all of it — because it monitors every recurring charge, every month, automatically.

Protection gap analysis: After a life event — a baby born, a marriage, a job change — the Twin evaluates whether your insurance coverage is adequate. “Your current life insurance is $250K. With a dependent, planning guidelines suggest $500K-$750K. Want me to get quotes?”

5. The Interface — “Talk To Me When It Matters”

The Digital Twin fundamentally changes what a banking app is for.

Today: you open the app to check balances and perform actions. The app is a tool. You are the operator.

With the Digital Twin: you open the app to review what the Twin did. The app is a report. The Twin is the operator.

The home screen isn’t a balance dashboard. It’s a Twin activity feed:

“Today: Moved $1,200 to 6-month CD at 4.2% ✓” “Today: Paid electric bill $87.40 ✓” “Yesterday: Negotiated fee waiver on Platinum card — saved $95/year ✓” “Action needed: Duplicate subscription detected — Spotify + Apple Music” “Milestone: Credit score reached 650 — mortgage pre-qualification unlocked”

You check this feed the way you check a good executive assistant’s daily report — trusting that the work is done, reviewing what matters, intervening only when judgment is needed.

The Twin only interrupts you for four reasons: it needs a decision that exceeds its POA scope, it completed a significant action worth noting, it detected a threat that requires your awareness, or you want to adjust your rules.

Everything else happens silently, continuously, in the background. The customer’s relationship with their bank shifts from “I use this tool” to “this agent works for me.”

The Trust Ramp: How Autonomy Is Earned

No rational person hands full financial autonomy to an AI on day one. The Digital Twin is designed for graduated trust — starting narrow and expanding as it proves itself.

Month 1: The customer activates the Twin with “Monitor only” across most domains. The Twin watches, learns patterns, and surfaces observations. “I noticed your CD matured last week and the funds are in a 0.01% holding account. A 6-month CD at 4.2% is available. Want me to move it?” The customer says yes manually. The Twin executes.

Month 2–3: After a few successful recommendations, the customer upgrades savings to “Recommend and act.” The Twin starts optimizing CD rates autonomously, notifying after each action. The customer reviews the activity feed, sees $180 in extra annual interest from rate optimization, and builds confidence.

Month 4–6: Bill payment gets upgraded to “Full auto” after the Twin has paid 3 months of bills without a single error. Subscription monitoring is activated. The Twin catches a duplicate streaming service and a price increase — saving $200/year. Trust deepens.

Month 6–12: The customer activates the Negotiation Agent for product offers. The Twin negotiates a fee waiver, a rate improvement on an existing account, and a better credit card match. Each successful negotiation builds more trust. Each decision the customer reviews and approves teaches the Twin more about their preferences.

Year 2+: The Twin is operating at “Recommend and act” or “Full auto” across most domains. The customer checks the monthly report, adjusts a constraint occasionally, and intervenes on major decisions. The Twin has generated measurable financial value: higher interest income, lower fees, better product terms, eliminated waste.

This trust ramp is the switching cost that no competitor can overcome. After 12 months, the Twin has learned the customer’s financial patterns, risk tolerance, constraint preferences, and optimization priorities. Switching to a competitor’s banking app means losing an agent that has been trained on a year of your specific financial behavior. That’s not a feature switching cost. It’s a relationship transfer cost — and people don’t transfer relationships with agents they trust.

Why This Changes the Economics of Banking

The Digital Twin doesn’t just improve the customer’s financial life. It restructures the economics of the bank-customer relationship.

For the customer: Higher interest income (the Twin constantly optimizes rates). Lower fees (the Twin detects and negotiates). Eliminated waste (the Twin catches subscriptions, duplicates, and erosion). Better products (the Twin matches spending patterns to optimal product terms). Financial protection (the Twin guards against fraud, creep, and coverage gaps). All without opening the app.

For the bank: Dramatically higher engagement — not through app opens, but through Twin-mediated interactions that generate behavioral data 24/7. Higher product acceptance rates — Twin-negotiated offers convert at multiples of standard banner offers because the terms are pre-optimized for both sides. Deeper relationships — the Twin creates multi-product customers who are virtually impossible to churn because leaving means losing the agent. Lower acquisition cost — the Twin’s performance data becomes the marketing message (“Customers with an active Digital Twin earned an average of $847 more per year”).

The commercial insight: The Twin aligns the customer’s interest and the bank’s interest structurally, not accidentally. When the Twin negotiates better terms for the customer, it simultaneously creates a deeper, stickier relationship for the bank. When the Twin optimizes the customer’s finances, it generates the behavioral data that makes the bank’s AI models better. When the Twin protects the customer from fraud, it reduces the bank’s loss rate.

Everyone wins. Not because of goodwill — because of architecture.

What This Means for the Future of Banking

I’ve been building digital banking for over a decade — across Vietnam, across Southeast Asia, across markets at every stage of digital maturity. And in every market, the fundamental model has been the same: the bank builds a better app, the customer uses the app, the bank measures engagement by app opens or app consumptions.

The Digital Twin ends this model.

The most engaged customer in the future won’t be the one who opens the app most frequently. It will be the one whose Twin is operating most actively — optimizing, negotiating, protecting, and reporting. They might open the app once a week. Their Twin interacts with the bank hundreds of times per day.

The bank that builds this first doesn’t just win a feature race. It creates a new category: agent-mediated banking. A category where the customer’s AI and the bank’s AI collaborate to optimize both sides simultaneously. Where financial health and revenue growth are the same motion. Where trust is earned incrementally, compounded daily, and virtually impossible to transfer.

The saffron merchant in bazaar built that relationship over thirty years of daily interaction, reading his customer’s needs, adjusting his offering, earning trust one transaction at a time. The Digital Twin builds it in siz to twelve months.

Same principle. Different scale. Same outcome: a relationship so deeply embedded that switching isn’t just inconvenient — it’s unthinkable.