There is a moment in every industry’s life cycle when the thing everyone assumed was valuable turns out to be infrastructure. It happened to telecommunications. It happened to cloud computing. It is happening right now to banking — and most bank CEOs haven’t noticed because the spreadsheet still looks fine.

Here’s the uncomfortable arithmetic. The marginal cost of underwriting a loan is collapsing. The marginal cost of detecting fraud is collapsing. The marginal cost of financial advice — real, personalized, context-aware advice that used to require a human with a CFA and a decade of experience — is collapsing. Not slowly. Not theoretically. Right now, in production, at banks that are paying attention.

A recent piece from Andreessen Horowitz examined how AI application companies are navigating brutal price wars — competitors undercutting each other weekly, margins evaporating, the constant temptation to discount your way to irrelevance. Their most striking finding had nothing to do with pricing tactics. It was this: across every enterprise buyer they spoke with, nobody chose a tool because it was cheapest. They chose the one that became indispensable.

That finding should terrify every bank executive reading this. Because it raises a question that no amount of cost optimization can answer:

when the core logic of banking becomes a commodity, what exactly is your bank selling?

The Price War You Can See

There are two wars happening simultaneously in banking. Most executives are aware of only one.

The visible war is straightforward. AI lowers operating costs. Banks compete on rates and fees. Margins compress. Every bank rushes to deploy AI-powered underwriting, robo-advisory, instant fraud detection, automated compliance. This is the race to the bottom, and it’s already underway. Within 24 months, every mid-tier bank will have these capabilities. Competing here is table stakes, not strategy.

But the invisible war is the one that matters. And it comes from a direction most bank boards aren’t watching.

The real competitor isn’t another bank. It’s the customer’s ecosystem becoming the bank.

When Grab/Uber embeds lending into its driver app. When Shopify offers instant working capital to its merchants. When VinGroup builds financial services into its retail and real estate platforms. When any company with transaction data and a developer team can assemble banking-grade services from APIs — using the same foundation models your bank uses — the licensed bank becomes invisible infrastructure. A utility behind someone else’s experience.

This is the “dumb pipes” scenario, and it’s worse than most bank executives realize. Big Tech doesn’t want to be a bank. They don’t want the regulatory burden, the capital requirements, the compliance overhead. They want something more dangerous: they want banking to be a feature inside their platform. A feature they control, a feature that keeps customers inside their ecosystem, a feature where the actual licensed bank is interchangeable and invisible.

The a16z research found that the most dangerous long-term competitor for AI app companies isn’t a rival startup — it’s the customer’s own engineering team asking “can we just build this ourselves?” In banking, the equivalent is every platform company asking: “why can’t we just embed this?”

The answer, increasingly, is: they can.

The Stickiness Illusion

Every Chief of Retail I’ve worked with has a version of the same comforting belief: switching costs protect us. Opening a new bank account is painful. Moving a mortgage is painful. Customers stay because leaving is hard.

This was true for decades. AI agents are about to make it false.

Picture this — and it’s not a thought experiment, because the infrastructure already exists. An AI financial agent that sits on your phone, connected to open banking APIs, continuously monitoring your mortgage rate, your deposit yield, your insurance premium, your credit card rewards, and your investment allocation. Not a comparison website you visit once a year. A persistent, autonomous agent that works for you, against every bank, twenty-four hours a day.

When your mortgage rate is 50 basis points above market, the agent doesn’t notify you. It initiates the refinancing. When a competitor offers a higher savings yield with equivalent protection, the agent (your digital twin with your POA) doesn’t suggest you consider it. It moves your money. When your credit card rewards structure is suboptimal given your actual spending patterns, the agent doesn’t send you a table. It applies for the better card and migrates your recurring payments.

This is the end of friction as a moat. The end of inertia as a strategy. The end of the assumption that customers stay because they chose to.

In this world, every bank’s “relationship” becomes a rolling auction. The CASA ratio that your board monitors as a proxy for customer loyalty? It becomes a lagging indicator of how long it takes for AI agents to optimize your customers out of your deposit base.

So what’s the defense?

It’s not better rates. An AI agent will always find a better rate somewhere. It’s not lower fees. Zero is the floor and everyone will hit it.

The only defense against an agent that optimizes for the customer across providers is becoming so embedded in the customer’s financial life that switching isn’t just painful — it’s structurally impossible. Not because of friction. Because of context.

The Context Moat

Every bank on earth has access to GPT-4, Claude, Gemini, and whatever comes next. The model is not the moat. It never was. The moat is what the model knows about this specific customer, right now, in context.

And this is where banking has an advantage that most bankers don’t fully appreciate — and that most technologists completely miss.

A bank that holds your salary account, your spouse’s business account, your mortgage, your children’s education savings, and your parents’ retirement portfolio — simultaneously — possesses a view of your financial life that no fintech, no Big Tech platform, and no AI agent can replicate. Not because the data is proprietary in some legal sense. But because the graph of relationships between these accounts creates intelligence that doesn’t exist anywhere else.

Your salary going into your personal account is a data point. Your salary going into your personal account while your spouse’s business revenue drops 20% and your mortgage payment increases and your son’s school fees are due next month — that’s a situation. A situation that demands a specific kind of intelligence: not generic financial advice, but deeply contextual understanding of a family’s financial architecture.

I call this the “Bank for Me, My Family and My Business” thesis. It’s not a marketing slogan. It’s an architectural principle. The bank that can reason across the full graph of a customer’s financial life — personal, household, and business, simultaneously — creates a context moat that no competitor can replicate by offering a better rate on a single product.

Peter Godfrey-Smith, the philosopher of biology, describes the octopus as a creature whose intelligence is distributed across its entire body. Each arm has its own neural cluster, processing information and making decisions semi-autonomously. But the arms are connected. Information flows back to a central brain that understands the whole organism, even as each limb acts independently.

This is the architecture a bank needs. Not a central AI brain that controls everything. Not eight disconnected AI features bolted onto a legacy core. A distributed intelligence where each capability — credit assessment, liquidity management, wealth planning, business advisory — processes information and acts with autonomy, but feeds into a substrate that understands the whole customer. The whole household. The whole business.

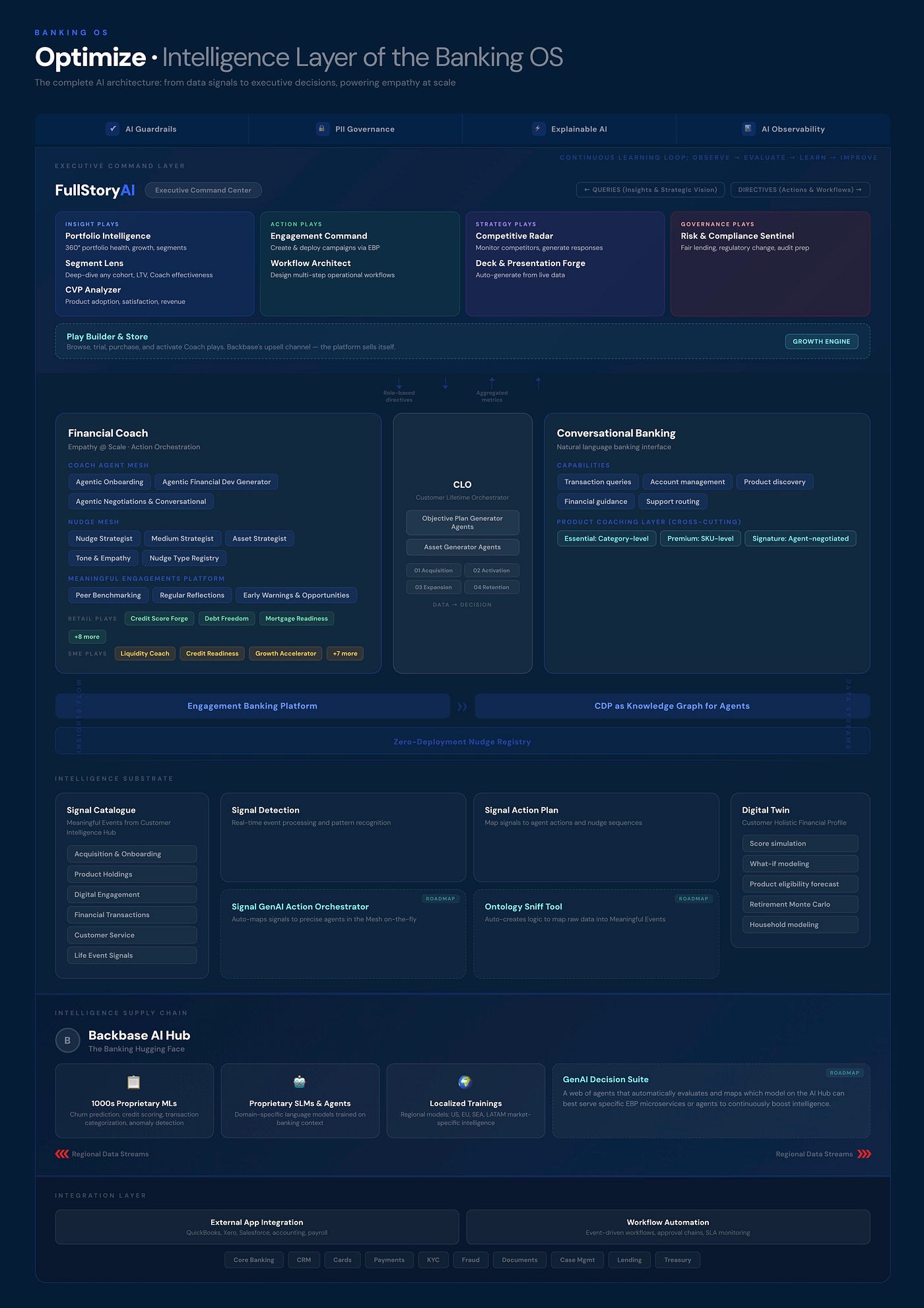

At Backbase, this is what we’re building with the Intelligence Layer of the Banking OS. Not because it’s a technology trend, but because it’s the only architecture that answers the price war question honestly.

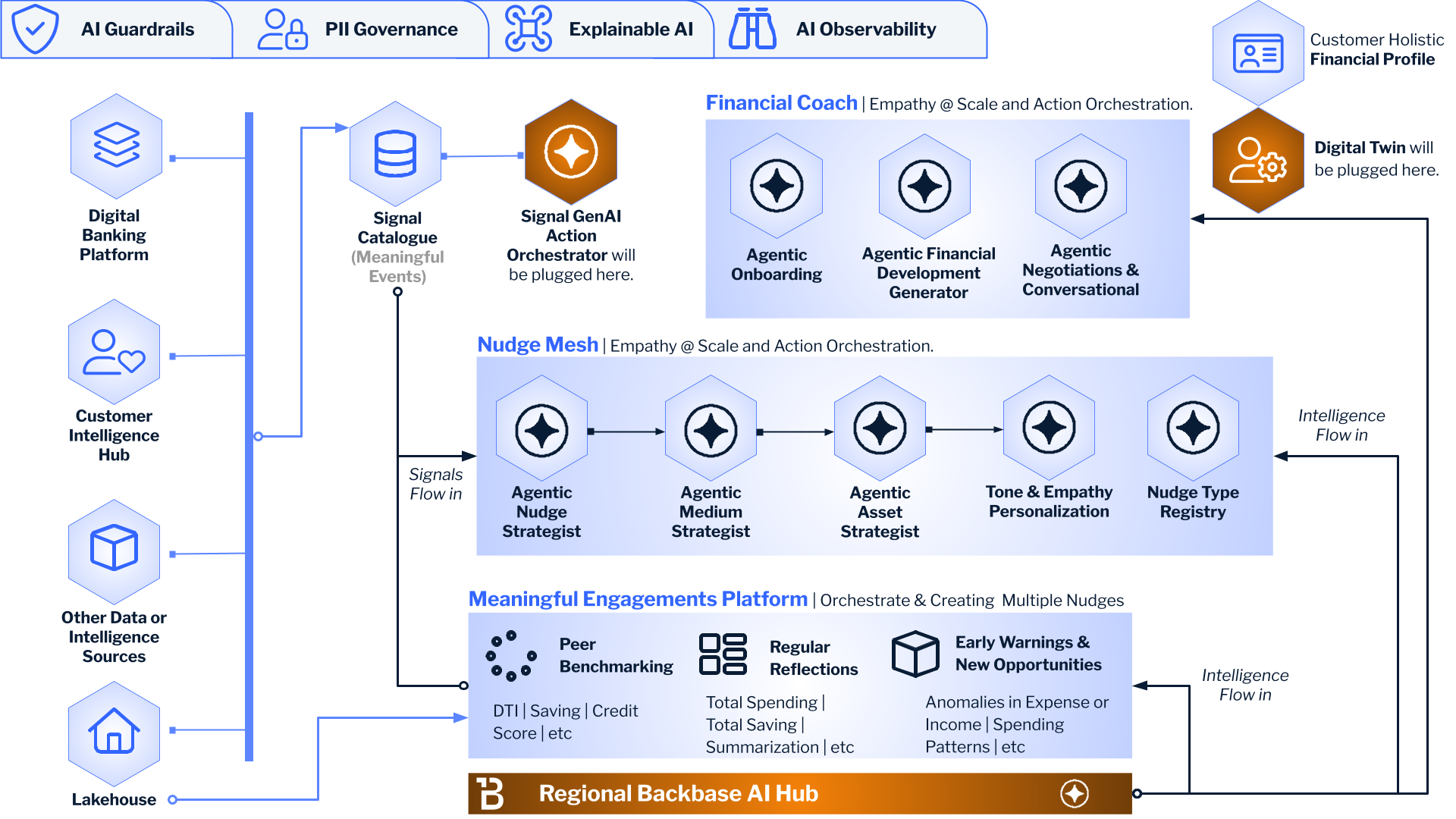

The Intelligence Substrate sits beneath everything: a Signal Catalogue ingesting meaningful events across acquisition, product holdings, digital engagement, financial transactions, customer service, and life-event signals. A Digital Twin — a holistic financial profile for every customer — enabling score simulation, what-if modeling, product eligibility forecasting, retirement Monte Carlo, and household modeling. A Signal GenAI Action Orchestrator that auto-maps signals to precise agents on the fly.

This isn’t a chatbot. It’s a nervous system. And the bank that builds it becomes the bank that an AI switching agent can’t easily replace — because no competitor has the same picture.

From Transactions to Trajectories

The current banking revenue model charges for two things: access (account fees, minimum balances) and events (wire fees, FX spreads, loan origination, trading commissions). AI compresses both toward zero. This is the “zero-margin bank” scenario, and fighting it with incremental fee optimization is like rearranging deck chairs.

The alternative is to charge for something AI makes more valuable, not less: the customer’s financial trajectory over time.

Consider how this works in practice. In retail banking, the Intelligence Layer powers a coaching architecture organized not by product but by customer life stage:

Entry plays build financial readiness. A Credit Score Forge for thin-file consumers and new-to-country immigrants. A Debt Freedom Engine for millennials with high debt-to-income ratios. A Resilience Shield for paycheck-to-paycheck workers and gig economy participants. These plays aren’t products. They’re on-ramps — the moment a customer starts moving toward a better financial position, the bank becomes the engine of that motion.

Deepening plays build the relationship. A Life Shift Navigator for adults facing major transitions — marriage, baby, divorce, job loss, inheritance. A Family Financial Orbit for multi-generational households managing shared finances. A Solopreneur Symphony for freelancers crossing the bridge from retail to SME banking. These plays are where the bank moves from utility to partner — from “where you store money” to “how you navigate life.”

Horizon plays lock in assets under management. A Freedom Glide Path for pre-retirees. A Mortgage Readiness journey spanning five to seven years. A Saving to Wealth pathway for first-time investors. These are the plays where lifetime value is captured — not through lock-in, but through demonstrated value over time.

The same architecture extends to SME banking: a Launchpad for formation and Day 1 structure → a Growth Accelerator for expansion → a Succession Compass for exit planning and wealth transition. A Liquidity Coach, a Credit Readiness Forge, a Business Resilience Shield — each play feeding the next, each transition deepening the relationship.

Underneath all of this runs a cross-cutting Product Coaching Layer with three tiers: Essential (category-level recommendations), Premium (SKU-level matching), and Signature (agent-negotiated, white-glove product placement). The pricing architecture mirrors the value architecture. Commodity banking is free or near-free — the loss leader that gets the customer into the coaching ecosystem. The plays that move a customer from debt to wealth, from startup to succession, from paycheck-to-paycheck to financial freedom — those are where margin lives.

This is outcome-based pricing applied to banking. The bank that charges for “a mortgage processed” will be undercut by AI. The bank that charges for “mortgage readiness achieved over a seven-year coaching journey” is selling something no competitor can price-match, because the value is in the relationship over time, not the transaction at a point in time.

Intelligence for the People Who Run the Bank

There’s a second audience for the Intelligence Layer that most AI strategies ignore: the executives who run the bank itself.

The same architecture that coaches customers must also coach the CEO, the Chief of Retail, the Head of Business Banking. This is FullStoryAI — not a dashboard, not a BI tool, but an executive intelligence system that receives queries (insights, strategic vision) and issues directives (actions, workflows) in natural language.

The plays are organized by what they do, not by topic. Insight plays — Portfolio Intelligence, Segment Performance Lens, CVP Effectiveness Analyzer — for understanding what’s happening across the customer base. Action plays — Engagement Command, Workflow Architect — for deploying targeted interventions through the Engagement Banking Platform. Strategy plays — Competitive Intelligence Radar, Deck and Presentation Forge — for anticipating market shifts and auto-generating board-ready analysis from live data. Governance plays — Risk and Compliance Sentinel — for continuous fair lending monitoring, regulatory change tracking, and audit preparation.

For the CTO and Chief of AI reading this: the Intelligence Layer is not a technology project. It is an operating model. It is the difference between a bank that uses AI to cut costs and a bank that thinks differently — where decisions that used to require weeks of analyst work happen in natural language, in real time, connected directly to action.

The Play Builder and Store deserves special attention. It lets the bank browse, trial, purchase, and activate new coaching plays — essentially an app store for banking intelligence. This is where the platform sells itself: new capabilities deployed without new code, new customer journeys activated without new projects, new revenue streams opened without new headcount.

Humans as the Luxury Layer

Here is the part that most AI strategies get exactly backwards.

The conventional wisdom says: use AI to make human advisors more efficient. Give them AI copilots. Summarize customer data before meetings. Auto-generate follow-up emails. This is fine. It’s also strategically irrelevant. It optimizes a model that’s about to be obsoleted.

The unconventional truth: in a world where AI provides excellent mass-market financial coaching — empathy at scale through the Nudge Mesh, peer benchmarking, regular reflections, early warnings and opportunities — human advisors become a status good. Not a service necessity. A luxury.

This isn’t a demotion. It’s a repricing.

The mass market gets the Financial Coach. Agentic onboarding, agentic financial development, agentic negotiations — all orchestrated through the Coach Agent Mesh, powered by the Nudge Mesh’s medium strategist, asset strategist, tone and empathy personalization. It’s better than what most human advisors deliver today. More consistent. More available. More patient. And it costs almost nothing per customer to operate at scale.

The affluent segment gets humans augmented by AI — advisors whose every conversation is informed by the Digital Twin, who walk into a meeting already knowing the client’s full financial picture across personal, household, and business dimensions, who can run what-if scenarios in real time. The advisor is the interface. The intelligence is the machine.

The ultra-wealthy get humans who use AI invisibly. The experience feels entirely bespoke and personal. The preparation is machine-grade. The client never sees the infrastructure. They only feel the quality.

This is the “Trust Premium” that the a16z piece hints at but doesn’t develop. In banking, trust isn’t just a brand attribute. It’s a pricing tier. The bank that understands this stops trying to automate every interaction and starts being strategic about where human presence creates margin.

AI for the many. Humans for the few. Intelligence for everyone.

The Uncomfortable Conclusion

The banks that survive the AI price war won’t be the ones that cut costs fastest. They won’t be the ones with the best chatbot, the slickest app, or the most aggressive fee structure.

They’ll be the ones that understood something early — something that the a16z research confirms across every industry they studied: when intelligence becomes cheap, the winners are not the companies that use it to do the same things for less money. The winners are the companies that use cheap intelligence to become structurally different.

For a bank, structurally different means this: a coaching architecture that accompanies the customer across every life stage. An intelligence substrate that reasons across the full graph of personal, family, and business finances. An executive command layer that lets the bank’s leaders think in real time. And a human layer that operates not as a cost center to be optimized, but as the premium tier where trust — the one thing AI cannot manufacture — commands its highest price.

The zero-margin bank isn’t a prediction. It’s a choice. You can race to the bottom on fees and rates, compete with every fintech on the commodity layer, and watch your margins evaporate quarter by quarter. Or you can build the architecture that makes your bank the one thing an AI agent can’t replace: the institution that knows the customer better than the customer knows themselves.

Most banks will choose the first path. They’ll call it “digital or AI transformation.” They’ll present impressive cost savings to their boards. And they’ll wonder, three years from now, why their best customers left without warning — optimized out of the relationship by an agent that found a better rate, a lower fee, a faster process.

The few that choose the second path won’t look like banks anymore. They’ll look like intelligence companies that happen to hold a banking license. Which is exactly the point.