Assembling the Pieces of a Puzzle

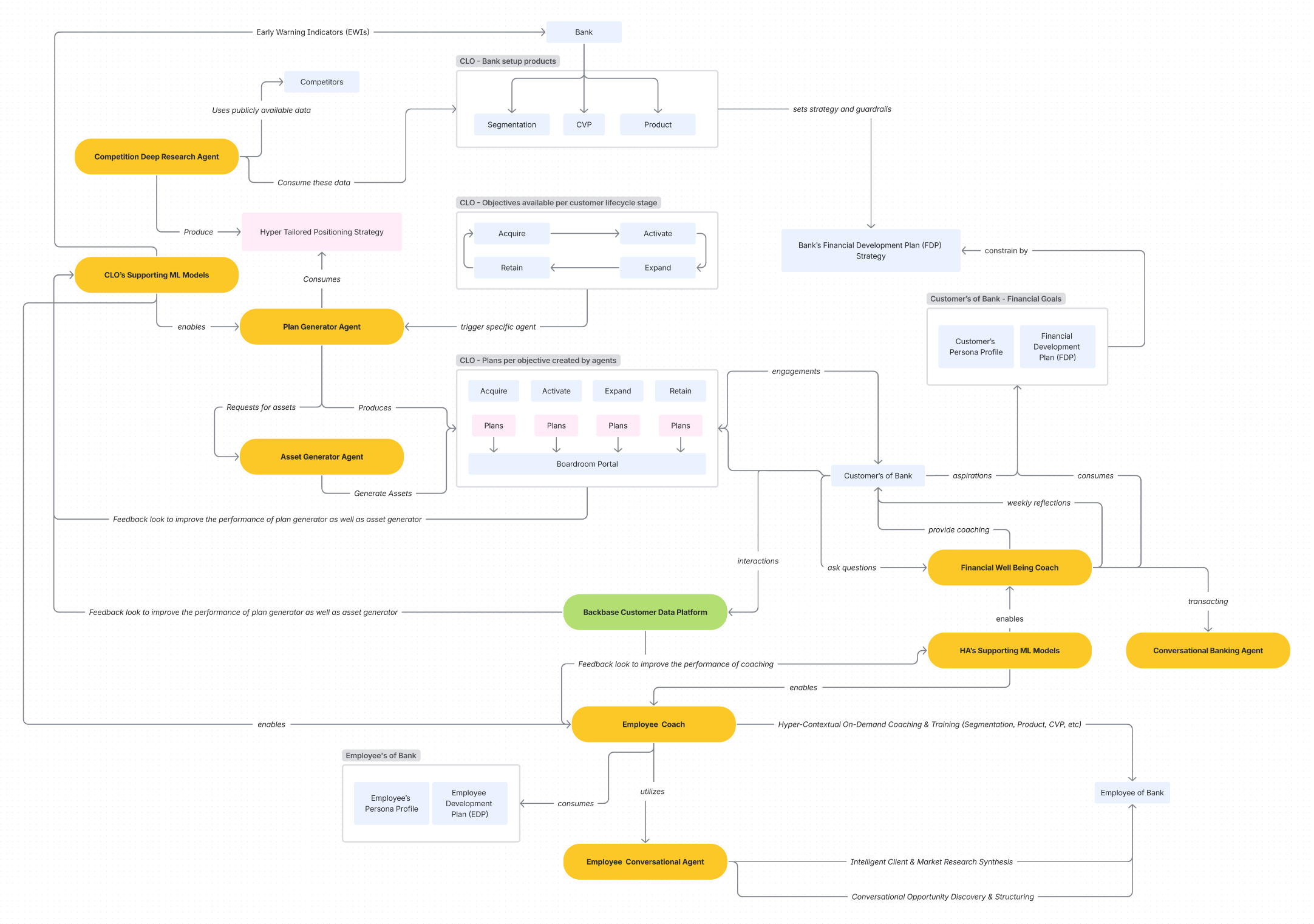

Your Chief Data Officer is building a Data Mesh. Your Head of AI is prototyping an “Idea Machine” to drive Customer Lifetime Value (CLV). Your Head of Digital is designing “augmented” co-pilots for your bankers. Each is a powerful, expensive, and critical initiative. And each is destined to hit a hard ceiling — or fail outright — unless they are recognized as components of a single, unified destination.

For too long, we have been building the engine, the plumbing, and the philosophy of a new bank in separate rooms. The data team works on their mesh, frustrated that their new “data products” aren’t being consumed. The AI team builds brilliant models that are starved for clean, real-time data, or fail the “last mile” test of trust and adoption. The digital team builds slick interfaces that are fundamentally “dumb,” lacking the deep, proactive intelligence to truly help the customer.

We are building faster horses, when the market is demanding a car.

These are not separate strategies. They are disconnected components of a single, unified machine. As separate projects, they will yield only incremental gains and diminishing returns. The “Idea Machine” is starved for fuel, and the “Data Mesh” lacks a “killer app” to justify its existence.

It’s time to connect the dots. This article is the capstone that assembles these pieces. These initiatives are not competitive; they are sequential. They are the essential components for the “Invisible Bank.” This ultimate vision, embodied by an autonomous “Financial Digital Twin” for every customer, is not another project. It is the final, unifying application that unlocks the true economic growth AI has long promised. It is the machine that turns your fragmented, multi-million dollar bets on data, AI, and digital into a single, cohesive, and revolutionary future.

Section 1: The Blueprint and the Foundation

To understand where we are going, we must first agree on why such a radical transformation is not just a “nice-to-have,” but an economic necessity. The days of growth-by-acquisition or expanding a physical branch network are over. For a mature industry like banking, the only remaining vector for sustainable growth is through deep, technology-driven innovation.

The Engine of New Growth

As I explored in my post, “Sustainable Growth from Nobel Ideas to AI,” the macroeconomic models of Nobel-winning economist Paul Romer argue that true growth doesn’t come from just adding more capital or labor. It comes from new ideas — new recipes that combine existing resources in more valuable ways. This is the “creative destruction” that drives an economy forward.

For the last two centuries, this innovation was a slow, human-led process. Today, we have a new, non-human engine for this process: Artificial Intelligence. AI, in this context, is not just a tool for automation; it is a foundational “amplifier” for innovation. It is a machine that can test billions of new “recipes” or ideas at a scale and speed no human team ever could.

For a bank, this is the non-debatable fact that justifies the entire technological shift. Your competitor is no longer just the bank across the street; it’s the FinTech startup that uses AI to create a novel lending product from scratch, or the tech giant that uses its data to offer a seamless payments experience. Without this new engine of innovation, banks risk becoming “dumb pipes” — low-margin, commoditized utilities in a financial ecosystem run by faster, more intelligent players.

The Factory Blueprint

If AI is the macro-engine, what is its specific application in finance? In “The Idea Machine and the Future of Finance,” I framed this as the blueprint for an “Idea Machine.” This is the “factory” inside the bank designed to automate financial innovation.

This factory’s theoretical purpose is to:

- Sense Need: Ingest vast, real-time data to identify a customer’s unspoken financial need (e.g., “This customer’s cash flow is becoming volatile; they are at risk”) aka Empathic Banking.

- Generate Ideas: Sift through thousands of product combinations, risk models, and market variables to generate a novel solution (e.g., “A 6-month, flexible micro-loan with a dynamic payment schedule based on their invoice cycle”).

- Deliver Value: Proactively offer this hyper-personalized, N-of-1 solution to the customer at the exact moment of need.

This is the promise. But for any bank leader who has tried to build this, the reality is a story of frustration. This powerful, expensive factory is stalled.

The Bottleneck. Starved for Fuel, Lacking Trust.

The “Idea Machine” is bottlenecked by two critical, systemic failures.

First, it is starved of “fuel” (data). The AI models are brilliant, but they are “deaf and blind.” The data they need to function is trapped in a Byzantine maze of 40-year-old core banking systems, siloed wealth management platforms, disconnected marketing clouds, and third-party card processing monoliths. An AI model trying to get a 360-degree view of the customer is like a chef trying to cook a gourmet meal by sourcing ingredients from five different, locked pantries, each with its own key, in a different building, and with no guarantee of what’s inside. The result is a model trained on stale, incomplete, and contradictory data. It can’t generate a truly “hyper-personalized” idea; it can only generate a slightly-better-than-average guess based on a bad dataset.

Second, it fails the “last mile” test of trust. Even if the machine could generate the perfect product, how is it delivered? A “black box” recommendation that suddenly appears in a banking app saying, “You should buy this derivative” isn’t helpful; it’s creepy. The customer has no context, no control, and no reason to trust the machine’s motives.

The Foundation. The Plumbing for the Factory.

This is where the Data Mesh comes in. As I detailed in “Data Mesh in Banking” and “Conquering Data Mesh Challenges,” this new data architecture is the only modern solution to the “fuel” problem.

A Data Mesh is not just another data lake or warehouse. It is a fundamental shift in philosophy. It dismantles the centralized data “monolith” and empowers individual business domains (e.g., “Mortgages,” “Small Business Lending,” “Card Services”) to own, clean, and serve their data as a “data product.”

This is the “Brain and the Nervous System” theme.

- The AI “Idea Machine” is the central Brain.

- The Data Mesh is the central Nervous System.

A brain, no matter how powerful, is useless without a nervous system to feed it real-time, high-fidelity sensory information from the world. A traditional data warehouse, with its 24-hour-old batch updates, is like a nervous system that only reports what happened yesterday. The Data Mesh, with its discoverable, interoperable, and real-time “data products,” is a nervous system that allows the AI brain to see, hear, and feel the customer’s financial life right now.

By solving the “fuel” problem, the Data Mesh provides the high-octane, reliable data stream the “Idea Machine” needs to function. It is the essential plumbing for the factory.

We now have the blueprint (Idea Machine) and the foundation (Data Mesh). But a factory with no “operator” or “business plan” is useless. It can’t just create ideas; it must create value.

Section 2: The Ghost in the Machine

A factory that can run at the speed of AI, powered by a constant flow of all-encompassing data, is an incredibly powerful, and dangerous, asset. What is its purpose? And who, or what, is in control?

This is where we must define the business plan and the operating philosophy for our machine. Without them, this powerful engine will either spin uselessly or, worse, drive the bank straight into a wall of regulatory and reputational ruin.

The “Goal”: The Factory’s Prime Directive

What is the factory for? What is its primary business objective? It’s not to sell more mortgages. It’s not to push more credit cards.

The prime directive for the 21st-century bank, as I argued in “AI-Driven Customer Lifetime Orchestration for Banks,” is the proactive orchestration of Customer Lifetime Value (CLV).

This is the “Unification of Value” theme. It represents a profound paradigm shift.

- The Old Model (Product-Centric): The bank is organized into vertical silos (checking, savings, loans) that compete for the customer’s business. The goal is to maximize the profit of each transaction. This is an adversarial, zero-sum relationship.

- The New Model (CLV-Centric): The bank is organized horizontally around the customer’s life. The goal is to maximize the long-term health and value of the entire relationship. This is a symbiotic, positive-sum relationship.

When the bank’s “Idea Machine” is aimed at CLV orchestration, its goals change. It stops asking, “How can I sell this customer a mortgage?” and starts asking, “What is the next best action I can take to improve this customer’s financial health, thereby deepening their loyalty and long-term value?”

Sometimes the answer is to sell them a mortgage. But other times, the answer might be to proactively tell them to refinance their mortgage with a competitor who is offering a rate the bank can’t match. This action, while losing a transaction, builds a level of trust and loyalty that guarantees the bank will win the next ten transactions.

CLV orchestration aligns the bank’s incentives with the customer’s. The bank wins when the customer wins. This is the only sustainable business model in an age of perfect information and zero switching costs. This is the business plan for our factory.

The “How”: The Philosophy of Trust

We now have an AI factory (Idea Machine), powered by a Data Mesh, with a clear business plan (CLV Orchestration). But one final piece is missing: the “operator.” How do we ensure this powerful machine, pursuing this intimate goal, solves the “last mile” trust problem that I identified in the “Idea Machine” article?

The answer lies in the operating philosophy. As I detailed in “Augmented Intelligence in Banking” and “Intelligent Banking — Beyond Automation,” the path forward is not Automation; it is Augmentation.

This is the “ghost in the machine.”

- Automation is a “black box.” It replaces a human. It’s cold, efficient, and opaque. It’s the automated “computer says no” loan denial. It’s the “creepy” ad that follows you. It breeds distrust.

- Augmentation is a “glass box.” It partners with a human. It’s an empathetic co-pilot. It provides “explainable” insights, context, and options, empowering the human (whether an employee or the customer) to make a better, more informed decision.

This philosophy must be the “soul” of our machine. It governs every interaction.

- For the Bank Employee: The “Idea Machine” doesn’t replace the wealth advisor. It becomes their co-pilot. It whispers in their ear, “Your client is 30 days from a major liquidity event. Here are three portfolio adjustments, complete with simulated outcomes and compliance checks, for you to discuss with them.” It gives the banker superpowers, making them more empathetic, productive, and valuable.

- For the Customer: The AI in their app doesn’t just act. It suggests and explains. It doesn’t say, “Your money has been moved.” It says, “I see you have a goal to save for a vacation. I’ve found a high-yield account that will get you there 45 days faster. Here is a simulation. Would you like me to set that up?”

Augmented Intelligence is the “how” that solves the trust bottleneck. It ensures the “Idea Machine” is not a “creepy overlord” but a trusted, fiduciary partner.

Now, all the pieces are finally on the table. We have the Foundation (Data Mesh), the Blueprint (Idea Machine), the Goal (CLV), and the Philosophy (Augmentation).

What happens when we turn on the power?

Section 3: The Invisible Bank

This is the moment of synthesis. This is the payoff for all the massive, disconnected investments.

The “Invisible Bank,” which I first outlined in “The Future of Banking is Invisible,” is not another idea in the sequence. It is the living, breathing embodiment of all the previous pieces working in concert.

The “Invisible Bank” is an evolution, moving the bank from a reactive chore (a place you “go to”) to a proactive coach (an AI that “helps you”), and finally, to an autonomous “Financial Digital Twin” — a true fiduciary agent that manages your financial life on your behalf.

This “Digital Twin” is the “killer app” the Data Mesh was built for. It is the final, perfected delivery mechanism for the “Idea Machine.” It is the ultimate expression of CLV Orchestration, all wrapped in a “glass box” of Augmented Intelligence.

Let’s assemble the machine, piece by piece.

The Twin is the Idea Machine, Perfected

The “Idea Machine” was a B2B concept — a factory for the bank to invent and push products.

The “Financial Digital Twin” is that same machine, but flipped 180 degrees. It is a B2C, N-of-1 agent that works for the customer. It doesn’t invent a product for a “segment” of 100,000 people. It orchestrates all available market products (from your bank and even third parties) into a perfect, dynamic solution for one single person.

This is the “From Factory to Fiduciary” theme made real. The bank’s “factory” is no longer a tool for selling. It is the engine that powers a digital fiduciary — an agent whose sole purpose is to act in its owner’s best financial interest.

The Twin runs on the Data Mesh

The Digital Twin cannot function on stale, siloed data. It would be like a self-driving car trying to navigate a new city using a 24-hour-old map.

The Twin is the ultimate consumer of the “data products” that your Data Mesh provides. Picture its daily “wake up” routine:

- It pings the “Customer Transaction” data product: “What is my owner’s real-time cash flow?”

- It pings the “Loan Portfolio” data product: “What are their current liabilities?”

- It pings the “Market Rates” data product: “Are there better interest rates available anywhere on the market right now?”

- It pings the “Customer Goals” data product: “My owner is saving for a house. Are they on track?”

This is the “Brain and Nervous System” in perfect harmony. The Twin (the brain) is completely dependent on the Data Mesh (the nervous system) to feed it a clean, real-time, 360-degree view of its owner’s world. Without the mesh, the Twin is lobotomized. With it, the Twin has a form of financial omniscience.

The Twin operates via Augmentation

This omniscient agent could easily be terrifying. But its entire relationship with the user is governed by the philosophy of “Augmented Intelligence”. It is the “glass box” defined.

It solves the “last mile” trust problem by prioritizing partnership and control.

- A Bad (Automation) Interaction:

ALERT: Your $5,000 has been moved to a new savings account.(This is alarming, creepy, and violates trust, even if it was the "right" move). - A Good (Augmentation) Interaction:

NOTIFY: "Hi Chris, I've been running simulations based on your 'emergency fund' goal. I found a new account that pays 1.5% more and is just as liquid. By my math, this will earn you an extra $75 this year. I've prepared the transfer and you can approve it with one tap. Would you like to know more about why I chose this one?"

This interaction builds trust. It explains its reasoning, links its action to a stated goal, quantifies the benefit, and gives the human the final control. Over time, as trust builds, the user may give it more autonomy: “You’re approved to make any moves under $1,000 that increase my yield by more than 1%.” The Digital Twin earns its autonomy.

The Twin executes the CLV Goal… By Ignoring It

Here is the final, beautiful synthesis. The Digital Twin is the ultimate “CLV Orchestrator”. But it achieves this goal by focusing entirely on the customer’s value, not the bank’s.

This is the “Unification of Value” brought to its climax.

The Twin’s prime directive is to autonomously and proactively maximize its owner’s financial health. It scans the market for better rates, it restructures small debts to improve cash flow, it sweeps micro-cents into investment accounts, it negotiates fees on its owner’s behalf.

By doing this, by being the single most valuable financial tool the customer has ever had, it generates a “gravity of loyalty” that is unbeatable.

Why would a customer ever leave a bank that provides them with an autonomous, personal, digital CFO that saves them time and makes them money every single day? They wouldn’t.

The byproduct of maximizing the customer’s value is the maximization of the bank’s CLV. Churn drops to near zero. Share of wallet becomes 100%. The relationship moves from transactional to essential. The bank has created a “fiduciary machine,” and the switching cost for the customer is now prohibitively high — they would have to fire their own personal financial brain.

The Inevitable. Invisible Bank.

The “Invisible Bank” is not a futuristic dream. It is not a 10-year science fiction project. It is the only logical, inevitable outcome of the strategic bets you are already making.

We have been building the components in isolation. We have been funding a Data Mesh initiative, an AI/CLV team, and a Digital “co-pilot” project as if they were separate endeavors. This fragmented approach is doomed to produce fragmented results: a well-built set of “pipes” with no water, a powerful “engine” with no fuel, and a beautiful “dashboard” with no intelligence.

Stop thinking of your Data Mesh, AI/CLV, and Digital Experience projects in isolation. Start seeing them as what they are: the foundation, the engine, and the operating philosophy for a single, unified, autonomous future.

The pieces are now assembled:

- Foundation: Data Mesh (The Plumbing)

- Blueprint: Idea Machine (The Engine)

- Goal: CLV Orchestration (The Objective)

- Philosophy: Augmented Intelligence (The Trust Protocol)

The “Invisible Bank” is the new operating system for finance. The “Financial Digital Twin” is its user interface. The strategic challenge for every bank leader is no longer if they should build these components, but how fast they can assemble them.

The first bank to successfully connect these pieces — to put the “Idea Machine” brain on the “Data Mesh” nervous system and wrap it in the “Augmented Intelligence” philosophy — will be the first to deliver a true Financial Digital Twin.

And that bank won’t just win market share. It will have redefined the market itself.